Mapping Scotland’s sustainable finance landscape

Research completed April 2026

DOI: https://doi.org/10.7488/era/7318

Executive summary

Scotland’s transition to a net zero economy presents a significant investment opportunity for renewable energy, green infrastructure and other sectors. Implementation of a net zero transition is complex and urgent. The scale of capital investment requires further significant mobilisation of private finance, alongside government investment. This report comes in response to a key recommendation of the Scottish Taskforce for Green and Sustainable Financial Services to produce an evidence-based report, mapping Scotland’s green finance landscape.

This report begins by examining available data on Scottish investment activity since 2020 in green infrastructure and renewable energy, with a minimum value of £10 million. The report then explores future investor appetite among finance institutions located or active in Scotland. It then examines green financial service provision from Scottish public/private initiatives and banks and funding institutions. It concludes by examining analytical methodologies that may further identify Scottish sustainable finance opportunities and gaps, as well as challenges in capturing future investment. The analysis adopts a mixed-methods approach, using commercial datasets and desk-based research alongside a limited number of targeted stakeholder interviews. The findings should be interpreted as indicative, as the start of a conversation on sustainable financing, rather than exhaustive.

Key findings and lessons learned

Key findings on Scotland’s sustainable finance landscape are:

- Approximately £9.5 billion has been deployed in green infrastructure and sustainable energy in Scotland since 2020; with the total annual investment increasing from £500 million in 2021 to £1.8 billion in 2023 and over £5 billion in 2025. This excludes Mergers and Acquisitions and deals under £10 million. This investment activity involved a broad mix of investors, including energy companies, commercial banks, infrastructure funds, institutional investors and public financial institutions.

- While investment activity has grown steadily since 2020 it remains concentrated in a relatively narrow set of mature sectors. For deals partly and fully located in Scotland, electricity transmission had the largest share of total investment (32%), followed by renewable energy (25%), and battery storage (21%). The largest investment sectors included renewable wind energy, electricity transmission and battery storage. These sectors benefit from more established technologies, clearer revenue models and strong policy support. Investment in emerging sectors such as industrial decarbonisation, low-carbon heat & transport and nature-based solutions appears more limited with some evidence suggesting higher risk perception and uncertainty of regulatory support and revenue models.

- Financial Services firms are undertaking a range of activities in this space, with key activities including capital allocation, portfolio management, advisory work and climate analytics.

- Financing structures appear to be dominated by debt financing, with 56% of the transactions analysed by the research financed by debt, bonds represented 35%. Equity transactions were relatively low, at 9%.

- The evidence suggests there are strong levels of further investor appetite for green investment in Scotland. Several asset managers, banks and corporate investors have announced plans for further Scottish investment, particularly in renewables, grid infrastructure and storage. Investment decisions tend to be made at a UK or global level rather than targeting Scotland.

- Public financial institutions play important roles across the financing lifecycle, providing patient capital and crowding in private investment. Institutions such as Innovate UK and the British Business Bank support early-stage, higher-risk innovation, while those such as the Scottish National Investment Bank and the National Wealth Fund support businesses as they mature through the crucial scale-up phase in providing patient capital and drawing in private capital.

- Initiatives such as the Global Ethical Finance Initiative and Transition Finance Scotland convene industry and public sector actors. Industry bodies and institutions (e.g. Scottish Financial Enterprise, Scottish Renewables and Scottish Futures Trust) support project development, market coordination and the identification of investment opportunities. Together, these stakeholders form an ecosystem that can support scaling of green investment in Scotland.

Lessons learned

The findings point to several key lessons for unlocking and mobilising greater flows of private capital in Scotland’s green sectors. Many of these challenges are structural, relate to ongoing challenges such as grid capacity, and the deployment of new types of financing. They include:

- Enhancing revenue certainty and policy clarity to reduce perceived investment risk, particularly in low-carbon heat and transport, nature-based solutions, and industrial decarbonisation. These areas are structurally challenging, and will require collaboration from across industry, academia, and government to address.

- Address infrastructure bottlenecks, particularly grid capacity, and improve the efficiency of permitting processes, as critical enablers of greater renewable energy investment. This is also a challenge which cuts across sectors, industry and government.

- More effectively target the use of blended finance and risk-sharing mechanisms to support early-stage and innovative projects where private finance still needs to be unlocked, including in sectors such as industrial decarbonisation, heat, transport and nature-based solutions.

- Explore mechanisms to attract and mobilise more risk capital into emerging green sectors, including venture capital and growth equity, to support innovation and the scaling of new technologies.

Next steps

The analysis presented in this report provides an initial evidence base and highlights areas where further research would support policy development. Further work could therefore build on this analysis to provide a more comprehensive review of Scotland’s green finance opportunities and constraints.

Potential next steps could include:

- Assessing Scotland’s green investment needs from a wider perspective, including sectors not covered in the current analysis, to include more detailed assessment of the scale of investment required to meet policy goals versus expected investment trajectories. This could help identify potential gaps between observed investment activity and sectoral investment needs to reach the net zero target.

- Undertaking a broader assessment of the factors influencing investor decision-making, including both barriers and drivers of investment, drawing on a broader range of stakeholders.

- Conducting a high-level assessment of emerging sectors such as hydrogen, carbon capture and storage, and nature-based solutions, including their investment readiness, project pipeline and key constraints to capital deployment.

- Exploring whether the current mix of financial products sufficiently supports businesses and projects across different stages of development. This would be particularly relevant for innovative or emerging sectors that may require financing between early-stage public support and conventional debt finance.

- Assessing where Scotland’s financial services ecosystem needs to develop further specified sustainable finance expertise to support future growth in green investment and identify opportunities for targeted skills development where gaps exist.

- Exploring approaches to diversify investment risk across green investment opportunities, helping to address challenges associated with project scale, concentration of capital and the limited ability of investors to diversify risks when investing in Scotland.

Glossary / Abbreviations table

BESS | Battery energy storage systems |

CCC | Climate Change Committee |

CCGT | Combined-cycle gas turbines |

CfD | Contract for Difference |

CPI | Climate Policy Initiative |

EV | Electric vehicle |

ESG | Environment, social, and governance |

ETF | Exchange-traded fund |

FDI | Foreign direct investment |

FCGFI | Flow Country Green Finance Initiative |

KPI | Key performance indicator |

LSEG | London Stock Exchange Group |

M&A | Mergers and acquisitions |

PuFin | Public financial institution |

TCFD | Task Force on Climate-related Financial Disclosures |

TRBC | Refinitiv Business Classification |

RQ | Research question |

NOA | Network Options Assessment |

NESO | National Grid Electricity System Operator |

NWF | National Wealth Fund |

OECD | Organisation for Economic Co-operation and Development |

R&D | Research and Development |

SNIB | Scottish National Investment Bank |

SNIFFER | Scotland and Northern Forum for Environmental Research |

SMEs | Small and medium-sized enterprises |

SPV | Special-purpose vehicle |

S&P | Standard & Poor’s |

UNCTAD | UN Conference on Trade and Development |

Introduction

Policy and strategic context

Private sector investment is crucial in the transition to net zero as well as addressing biodiversity loss and broader environmental pollution in Scotland. It requires the greening of key economic sectors alongside the development of new green industries. With an ambitious target of reaching net zero emissions by 2045 (Climate Change (Emissions Reduction Targets) (Scotland) Act 2019, 2019), Scotland offers strong investment opportunities in its transition to a more sustainable economy. Its draft Climate Change Plan 2026-2040 envisions that decarbonisation contributions from the transport, energy supply, business and industrial processes sectors will be particularly important (Scottish Government, 2025b).

The transition is already making a significant contribution to the Scottish economy. One economic model estimates that 105,000 jobs and £10.2 billion in economic value are currently supported in sectors such as energy, manufacturing, engineering and professional services (CBI Economics, 2026).

Reaching net zero requires further substantial, sustained and targeted investment. The Climate Change Committee (CCC) predicts that the cost for Scotland alone will be £145 billion between 2020-2050, equating to a £5.6 billion investment need per year between 2026-2040 (Scottish Government, 2025a). The Scottish Fiscal Commission estimates that around £41 billion of total investment is expected to come from public sources (Scottish Fiscal Commission, 2024). With public sector finances under sustained pressure, private sector investment is pivotal to achieving the transition. The Climate Change Committee estimates that 65-90% of the UK net zero financing required between 2025 and 2050 will need to come from the private sector (Climate Change Committee, 2025).

Following the success of the United Nations Climate Change Conference (COP 26) in Glasgow, in 2021, the Scottish Government announced an industry-led taskforce to develop an action plan to capitalise on the opportunities of financing the global shift to net zero. This resulted in the Scottish Taskforce for Green and Sustainable Financial Services (“the Taskforce”), which was convened by the Global Ethical Finance Initiative (GEFI) with funding from the Scottish Government. The Taskforce aimed to strengthen coordination within Scotland’s sustainable finance sector and position the country as a leading global hub for green and sustainable finance (GEFI, 2024b).

Scotland has well-established strengths in financial services and increasingly in sustainable finance (The Investment Association, 2024). Its financial ecosystem comprises global institutions, international companies alongside small, locally based companies (GEFI, 2024a). In the 2022/23 PwC Green Jobs Barometer, Scotland had the highest proportion of green financial job openings (PwC UK, 2023; Scottish Financial Enterprise, n.d.; Scottish Financial News, 2025).

Scottish Financial Enterprise aims to build on these strengths and to double assets under management in Scotland’s financial services sector, to £1 trillion by 2030 (Scottish Financial Enterprise, n.d.). However, the share of assets under management in the UK managed by investment managers from Scotland fell to 17% in 2023 from 26% in 2013. This was attributed to merger and acquisition activity among Scottish firms and the relatively faster growth of assets managed in London, among other factors (The Investment Association, 2024). Research by the Productivity Institute also indicated private investment in the Scottish economy was lower than other top-performing countries and lower than the wider UK in areas such as Research and Development (R&D) (D. Williams et al., 2025).

Scotland’s Green Industrial Strategy identifies four key areas where Scotland has existing strengths, that are most likely to lead to growth and with export potential (Scottish Government, 2024). These are: (i) maximising the wind energy economy, (ii) developing a self-sustaining carbon capture, utilisation and storage (CCUS) sector, (iii) growing the hydrogen sector, and (iv) establishing Scotland as a competitive centre for the clean energy intensive industries of the future. The strategy also advocates for additional public support to green economy financial services to support growth in these sectors.

By providing patient capital, helping to mobilise private finance and accelerating growth in priority green sectors, public financial institutions play a role in the net zero transition. For example, the Scottish National Investment Bank (SNIB) in its Investment Strategy for 2025-2026 positions itself as a patient capital investor focused on crowding in private capital seeking to invest in sectors contributing to net zero (Scottish National Investment Bank, 2025). The National Wealth Fund and Great British Energy also target green sectors.

Research commissioned by Skills Development Scotland and published in 2023 estimated that “green investments” taking place or expected to take place in 2025-2026 amounted to around £90 billion, with £48 billion of that “already going ahead or with a high likelihood of proceeding in the next 2-3 years” (Skills Development Scotland, 2023, p.4). This includes investments targeted in energy, transport, construction, manufacturing, agriculture and land use. However, no other recent studies have been identified which estimate investment levels in green sectors in Scotland or via Scottish financial institutions.

The environment in which sustainable investors operate continues to evolve, both in the UK and globally. Investment sentiment has been affected by the Russian invasion of Ukraine and instability in the Middle East has been driving up fossil fuel and other input prices, leading to concern over energy security and affordability. According to the Investment Association, some sustainable investment strategies affected by these developments generally delivered lower returns (The Investment Association, 2024).

In this context, the Taskforce report outlined how Scotland can position itself as a global green finance centre, but noted further work was needed to map the Scottish financial services landscape (GEFI, 2024a). This included exploring past investment trends, potential future developments and offerings of current green financial services. It noted this work would help the Scottish Government attract more green finance. This report is the first step in this direction, aiming to provide a baseline mapping of the green finance landscape in Scotland over the past five years.

Research questions and methodology

This research outlines the sustainable financing landscape in Scotland, as per the Taskforce recommendation. The goal is to understand which institutions have invested in Scotland, in which sectors and which types of projects over recent years. The study also evaluates available information on investors’ interest in Scotland in the short and medium-term future. It seeks to answer four research questions (RQs):

- Which private and public institutions have completed deals for investments over £10 million in Scottish green infrastructure and renewable energy projects since 2020? (RQ1)

- Which financial institutions are looking to meaningfully structurally invest in Scottish projects in the short and medium-term future? (RQ2)

- Which funding institutions and initiatives operating in Scotland provide green financial services? (RQ3)

- What methodologies should be used to identify the opportunities that could be leveraged, the gaps, and challenges for future investment? (RQ4)

To answer these questions, we used a mixed-methods approach. To answer RQ1, we used data on past investment deals derived from the London Stock Exchange Group, (LSEG Data & Analytics), and from Standard & Poor’s (S&P) Global databases. These are specialist and comprehensive data providers who maintain the largest financial databases commonly used in academic financial analysis. This was complemented with desk-based research on Scottish investments and financial organisations. To answer RQ2, we further researched company websites and public documents where these contained stated plans and/or announcements on investing in Scottish green sectors. To answer RQ3, we analysed the green financial instruments and services that larger financial service providers located in Scotland currently offer. This report provides an overview of their green targets, commitments and associated strategies towards sustainable investment, based on publicly available information.

To supplement the desktop research, we conducted interviews with eight selected stakeholders representing the key investor types, including banks and asset managers. These stakeholders represented public and private markets as well as trade associations. The interviews gathered information on both past activity and the future plans of the institutions to support analyses for RQ 1, 2 and 3. Due to our sample size, sentiments expressed should not be considered to be fully representative of the wider investment landscape. To answer RQ4, we reviewed methodology guidance documents from various international institutions. A more detailed summary of our methodology is in Appendix A. Whilst this research is not a comprehensive nor exhaustive overview of the sustainable finance landscape in Scotland, it is intended to serve as a starting point for future research.

Definitions adopted in the study

- For the purposes of this study, “investment” in Scottish companies refers to the provision of capital through equity, bonds and loans, or mergers and acquisitions, where a target company or underlying assets are located in Scotland.

- This study adopts the definition of “Green Finance” which was developed by the Taskforce. This states “Green finance refers to any financial initiative, strategy, product or service designed to protect the natural environment and support the transition to a sustainable, low-carbon world, and/or to manage climate-related and other environmental risks impacting finance and investment” (Final Report, Scottish Taskforce for Green and Sustainable Financial Services, 2024, p. 12).

- Where there was uncertainty about whether an investment activity falls within the above definition, we referred to specific technical definitions in the EU Sustainable Finance Taxonomy (European Commission, 2026). Excluded investments judged to be outside the scope of the project were: (i) electric vehicle (EV) manufacturing, (ii) activities associated with oil supply for wind turbines, (iii) electric coach services, and (iv) smart meters. Although these investments may be classified as “green”, RQ1 focussed on renewable energy and green infrastructure.

- Further definitions used in the study relating to for green financial service providers, green instruments, services and finance initiatives are in Appendix B.

Limitations

There is a variety of definitions of green activities within the field. While this report adopts a specific framework and definition, the research may reflect different stakeholder perceptions which may result in slight variations in how the data are interpreted.

The research is unlikely to have identified all relevant deals, especially those which would be considered to constitute lower value deals, activities of small private firms or self-financed projects. To mitigate this, we complemented and cross-checked the information from databases with alternative public sources and news coverage as far as possible. Quantitative data is also supplemented with stakeholder interview evidence. Whilst this qualitative information provides additional detail and context, these insights are neither comprehensive nor necessarily representative of the institutions described in the study or the wider market.

Some investments were only partially located in Scotland, and it was not possible to determine the precise share could be attributed to Scotland. For example, an investment in electricity grids connecting Scotland and the rest of the UK may not specify the share of the total amount spent in Scotland. In other cases, a company may list projects in the UK, including Scotland, but may only publicly state total investment values, not individual amounts. To address this, investments were split into those “fully” and “partially” located in Scotland. It is recognised this is not a precise exercise but is intended to aid interpretation of the available data.

The databases used in the analysis include bonds, debt, equity (see Appendix B for definitions), as well as mergers and acquisitions. However, the databases do not include project equity investments where projects were financed from the balance sheet of a company. In cases where a specific deal reference or location was not explicitly identified within the database, the screening process focused on transactions where the investing or issuing company was headquartered in Scotland. Further desk-based research was then conducted to identify additional information on the underlying projects to confirm whether the investment was linked to projects located in Scotland. However, the UK-level deals may include activity in Scotland which is not captured by the approach taken in this study.

Furthermore, this study focuses on past deals in green energy and infrastructure over £10 million only. Also, it does not capture some broader elements of demand for green investment, such as in energy and energy efficiency.

For details on future investment plans, we have relied on information in the public domain, which may be outdated, incomplete, subject to change and limited in detail given commercial confidentiality and competition. Whilst interviews with stakeholders sought to mitigate this, at least some relevant commercially sensitive information will not be publicly available. Hence, the analysis is likely to reflect the lower end of a true level of investment.

Additionally, a total of eight interviews were conducted, and one institution provided a written response. As the sample size is not statistically representative, the input gathered does not provide a robust reflection of the views of all market participants. Among the interviewed organisations, there were banks (3), asset managers working either in private (2) or in public (1) markets, or both (1), and one trade association. Of the three banks, all are UK-based, with one headquartered in Scotland. The names of the institutions interviewed are not provided. They were selected to include large UK retail and commercial banks, and globally active asset managers.

The analysis of deal activity should be interpreted as indicative rather than exhaustive. It is based on a defined methodological scope, including the use of a dataset (LSEG), complemented by desk-based research and stakeholder interviews. While this approach improves coverage, it remains focused on transactions that are publicly disclosed and meet the study criteria (e.g. deals above £10 million). As a result, certain types of investment activity are not captured, including balance sheet financing. An alternative methodology and data coverage might produce a different but overlapping sample of deals, but the overall trends and aggregate investment values appear broadly consistent across data sources identified.

Investment activity in Scotland’s green sectors since 2020

Introduction

This section analyses completed deals in green infrastructure and renewables over £10 million in value in Scotland since 2020. It identifies patterns in scale, instruments, participating actors and other investment characteristics, alongside further insights from interviews. Further detail on data and methodology is reported in Appendix A.

Data for this section are drawn primarily from the LSEG Data & Analytics using the Sustainability flag incorporated into the database to identify green bonds, green loans, equity issuances and mergers and acquisitions of green Scottish companies. We then cross-checked and complemented the data with desk-based research drawing on public sources, company press releases, investor announcements and industry publications. A full list of sources for the desk-based research is reported in Appendix A.

In total, summing bonds, equity, debt and mergers and acquisitions of Scottish companies, we identified 54 deals between January 2020 and February 2026, with a combined amount of £9.8 billion. This figure captures only private capital market transactions (equity, loans, bonds and M&A involving Scottish companies where Scottish companies were acquired). Excluding M&A the figure is £9.5 billion.

Background

Climate-related investment is significant in both Europe and the UK, although consistent data on green investment is difficult to identify. European Union (EU) level investment averaged around €764 billion per year in activities that reduce greenhouse gas emissions between 2011 and 2020 (European Central Bank, 2025). At UK level, the Office for National Statistics estimates the UK low carbon and renewable energy economy amounted to £77 billion in 2024, an 11.8% increase on 2023, with Scotland accounting for £13.3 billion or one sixth of this total (Office for National Statistics, 2026). Note these figures are not directly comparable to the £9.8 billion estimate of investment in Scotland outlined above and the £48 billion projected by Skills Development Scotland outlined in section 3.1. They include public expenditure, infrastructure programmes and operational capital investment that fall outside the scope of deal data that we collected.

A core ambition in Scotland is to strengthen its contribution to total UK assets under management, putting green and sustainable finance as a core pillar of this growth (GEFI, 2024). This provides context for analysing our dataset of completed green deals in Scotland since 2020, capturing a narrow but growing share of private green investment flows.

Overview of green deals, 2020-2026

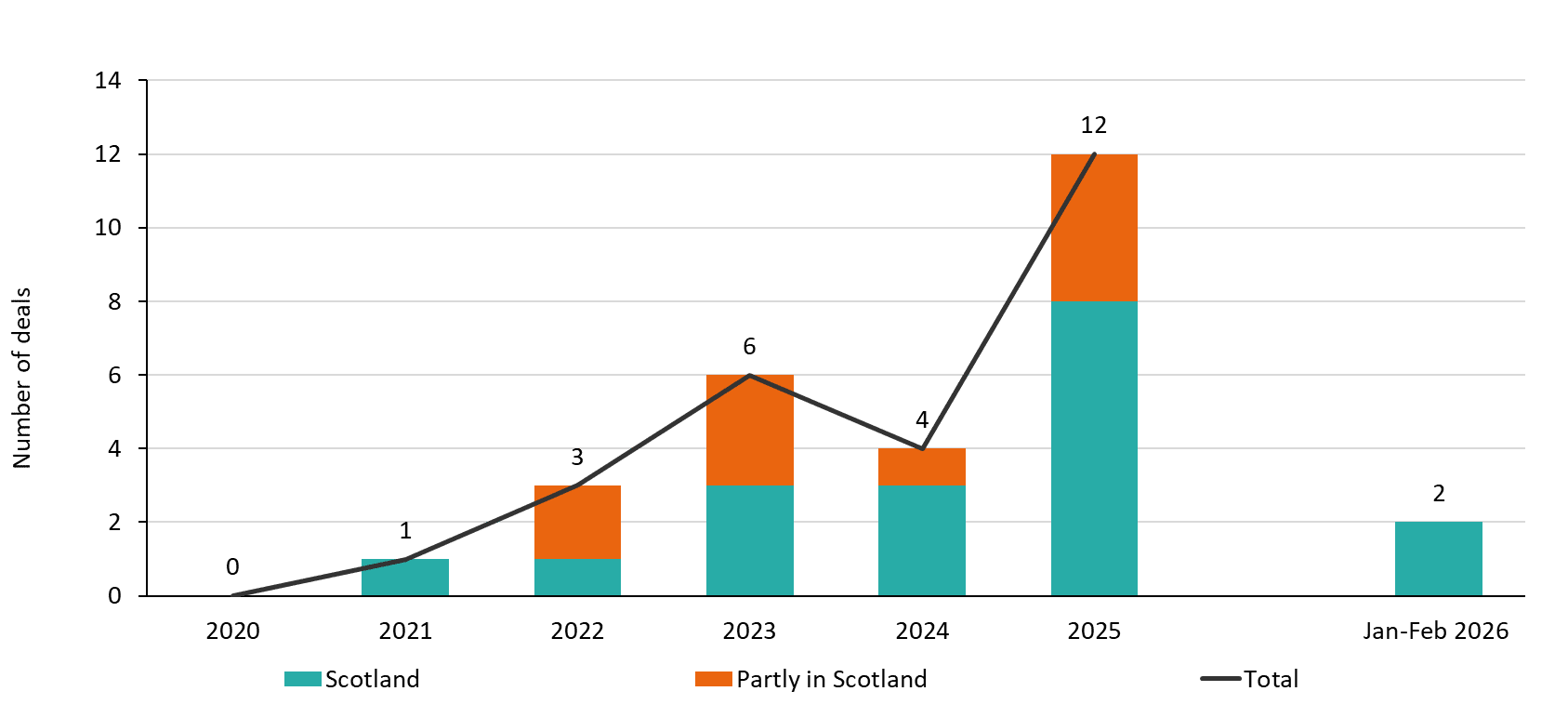

Figure 1 reports the number and annual volume of completed deals over £10 million identified in the research, focusing on bonds, equity and loans only. In total, we identified 28 deals which had completed since 2020. These deals were in green infrastructure and renewable energy as defined in LSEG. They include investments in sectors such as renewable energy, clean infrastructure, hydrogen, carbon capture, electric vehicles and renewable utilities (refer to Appendix B for more detail on the definition). The analysis was deliberately scoped to these sectors, applying a minimum £10 million deal size threshold to identify qualifying transactions. Focusing on equity and debt (loans and bonds) financing transactions, no relevant deals were recorded in 2020, likely reflecting the disruption and economic uncertainty associated with COVID-19. Investment activity for these deals has grown steadily since 2021, with a peak of 12 deals in 2025. For completeness, we included the deals reported in January and February 2026. As a result, 2026 is partial and not directly comparable with the previous years. These figures capture only discrete private capital market transactions, excluding investment financed directly from firms’ own balance sheets and are based on the methodology set out in Appendix A.

We interviewed stakeholders active in Scotland’s financial industry for comment on investment trends in these sectors. These included large UK-based retail and commercial banks, globally active asset managers (across private and public markets), infrastructure investors, and a leading industry body. One reported that investment in Scotland’s renewables and green infrastructure has grown but remained concentrated in a relatively narrow set of mature sectors, largely driven by project opportunities (source – interview with a bank). Public interventions, including subsidies, are seen to be playing an important role, particularly in de-risking capital-intensive projects, but several interviewees felt that inconsistent policy signals have constrained broader investment expansion (source – interviews with two banks, an asset manager (private markets), and a trade association). While specific policy instruments were not always explicitly identified, stakeholders indicated that gaps in long-term revenue certainty and pipeline transparency remain key constraints.

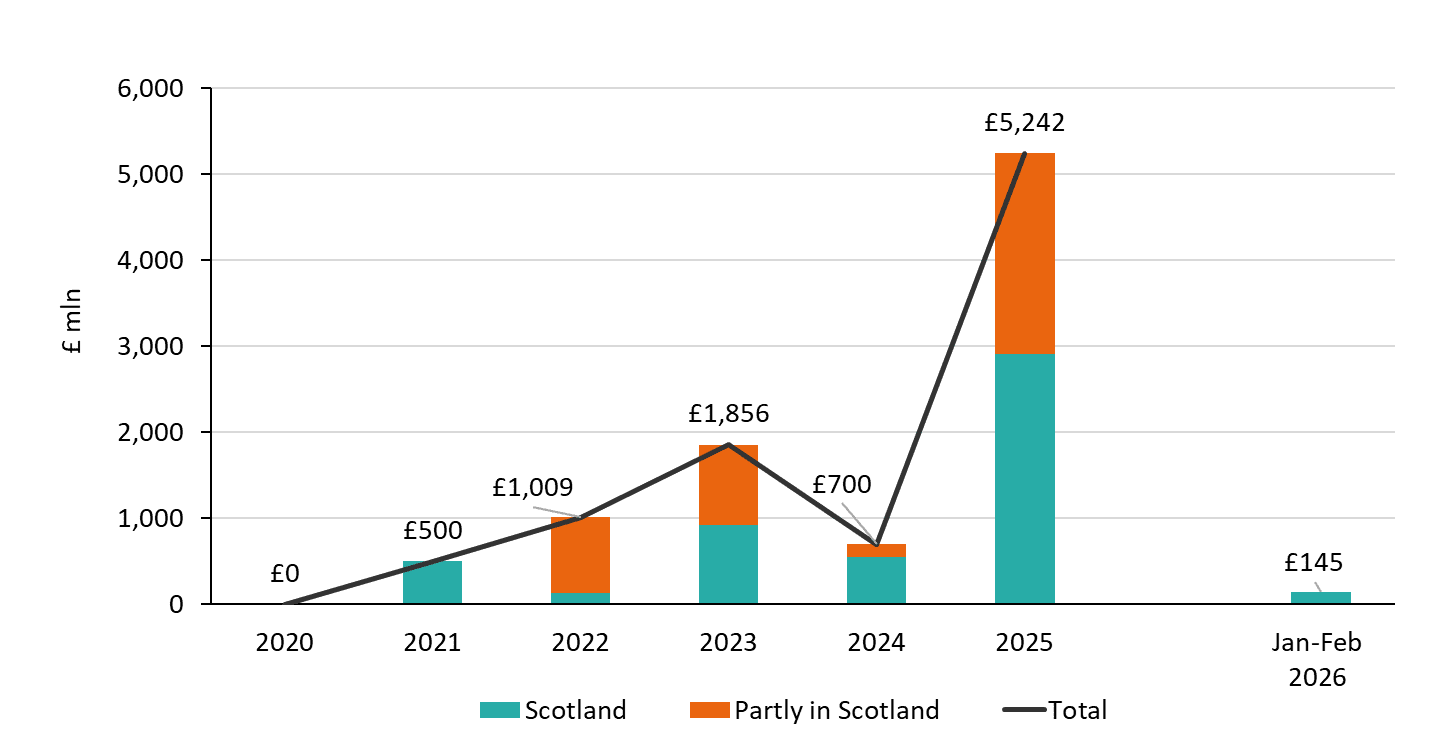

As of the end of February 2026, a combined value of around £9.5 billion has been invested in green deals which involve Scotland since 2020, excluding M&A. The total annual investment reached around £500 million in 2021, increasing to around £1.8 billion by 2023 and to over £5 billion in 2025. To provide context, approximately £5 billion per year of combined public and private investment is estimated to be required by the end of this decade to meet a balanced pathway to net zero for Scotland (R. Watts, 2024).

It is important to note that the total amount includes deals both fully and partially located in Scotland. The share of value attributable to Scottish assets in the latter is not disclosed. Despite this limitation, these deals are retained in the analysis to provide a full picture of the number and sectoral distribution of deals (see Section 4.4below). As a result, the total value figure may overstate the amount attributable solely to Scotland somewhat. Therefore, details of deals fully located in Scotland are also provided.

Figure 1 and Figure 2 report the number and monetary value of deals, respectively. These include deals fully located in Scotland (64%) versus deals partially located in Scotland (36%), respectively. Note, deals fully located in Scotland refer to deals where all investment activity is in Scotland. Deals partially invested in Scotland refer to deals forming part of a wider UK investment where the Scottish share of total value is not separately disclosed and the boundary of the investment extends beyond Scotland to the rest of the UK. In a small number of cases these deals also extend beyond the UK itself. In 2024, over three-quarters of deals were fully located in Scotland.

To contextualise the scale of these figures, it is useful to set them against wider investment activity in Scotland. The Scottish Government’s total capital budget stood at £6.2 billion in 2024–25 (R. Watts, 2024), of which around £2.2 billion was classified as low-carbon capital investment (Scottish Government, 2022). This means that private green investment in each year since 2021 in our sample has exceeded green public capital investment in 2024-2025. On the private side, total private equity investment across all sectors in Scotland reached £9.4 billion in 2024 (G. Williams, 2025). Note these figures are not directly comparable to our sample. They encompass a much broader cross-section of sectors and deal types, but provide confidence in the estimate from the sample, as these deals will likely comprise only a proportion of the total private capital deployed in Scotland each year.

The number of published deals is relatively small but steadily growing. This trend is likely to reflect macro conditions. Survey evidence from the Bank of England shows strong economic contraction and high volatility at the UK-level during and following the COVID-19 crisis. In contrast, some evidence suggests that the energy price shock following the Russian invasion of Ukraine in 2021-2022 may have boosted green investment intentions (Bank of England, 2024). The Bank’s survey response at the UK-level reports a growth of approximately 40% in green investment intentions between 2021 and 2023.

Figure 1. Number of completed deals in green infrastructure and renewables in Scotland 2020-2026 – loans, bonds, equity

|

Source: LSEG databases and desk-based research.

Figure 2. Volume (£ million) of completed deals in green infrastructure and renewables in Scotland 2020-2026 – loans, bonds, equity

Source: LSEG databases and desk-based research. Note: for deals that are only partly located in Scotland, the reported deal amounts reflect the total value of the larger, international or UK-wide transaction, rather than the share corresponding to Scottish assets.

Table 1 reports cross-border M&A activity, which given its specific nature, is presented separately. The analysis covers acquisitions of Scottish-headquartered companies only; acquisitions made by Scottish companies of targets located elsewhere were excluded.

Observing data on M&A deals involving the acquisitions of green companies in Scotland 2020-2026 provides context to inward foreign direct investment trends, and the attractiveness of Scottish green companies. The data show a total M&A deal value of £307 million, which represents foreign and British companies investing in Scottish assets (so called “pure-play M&As” only) rather than necessarily new physical capital expenditure within the country. The energy and power sector consistently leads in both the number of deals and average deal value, with a notable spike in deal value in 2020 at £162 million. In contrast, the industrials sector has more limited activity, with just one deal in 2024 and 2025 respectively.

Table 1: Average M&A deal value amount per sector and per year

Number of deals | Average of deal Value (GBP, Millions) | |||

|---|---|---|---|---|

Year | Energy and power | Industrials | Energy and power | Industrials |

2020 | 3 | 162 | ||

2021 | 3 | 6 | ||

2022 | 5 | NA | ||

2023 | 3 | NA | ||

2024 | 5 | 1 | 10 | NA |

2025 | 4 | 1 | 29 | 100 |

2026 | 1 | NA | ||

Total | 24 | 2 | 207 | 100 |

Source: LSEG databases and desk-based research. Note: some of the M&A deal amounts are not disclosed in the LSEG dataset. They are listed as NA in this table.

Sectoral distribution

The available data on sub-sectoral distribution remains highly uneven. The evidence suggests a trend toward mature, de-risked technologies. This suggests sectors critical to longer-term climate goals may face investment barriers driven by scalability constraints, uncertain demand and insufficient revenue certainty. This poses a challenge to longer-term decarbonisation ambitions.

Across Scotland’s green infrastructure landscape, stakeholder perspectives reveal a market where capital has flowed mostly into mature, revenue-certain technologies, while emerging sectors continue to face structural barriers for new investment. Interviewees noted that investment activity in renewables and green infrastructure in Scotland had been concentrated in more established sectors, particularly off- and onshore wind, hydro and increasingly in grid infrastructure and storage. Multiple interviewees noted fixed offshore wind as the dominant area of capital deployment but noted growing interest in enabling infrastructure such as transmission networks and battery storage (source – interviews with two banks, an asset manager (private markets), and a trade association). They viewed a notable gap in areas such as hydrogen and nature-based solutions, where uncertainty around revenue models and market structures was perceived to have constrained investment appetite (source – interviews with an asset manager in public markets, and an asset manager in private markets). Also, although peatland and woodland carbon markets in Scotland are considered relatively mature, the National Strategy for Economic Transformation (NSET) has committed to developing a “high-integrity, values-led market” for responsible investment in natural capital (GEFI, 2024a). Similarly, some interviewees noted retrofitting and energy efficiency initiatives in the built environment had struggled to scale due to weak end-user demand and a lack of compelling financing propositions (source – interviews with two banks). These patterns, drawn from stakeholder experience, are broadly corroborated by the deal-level data.

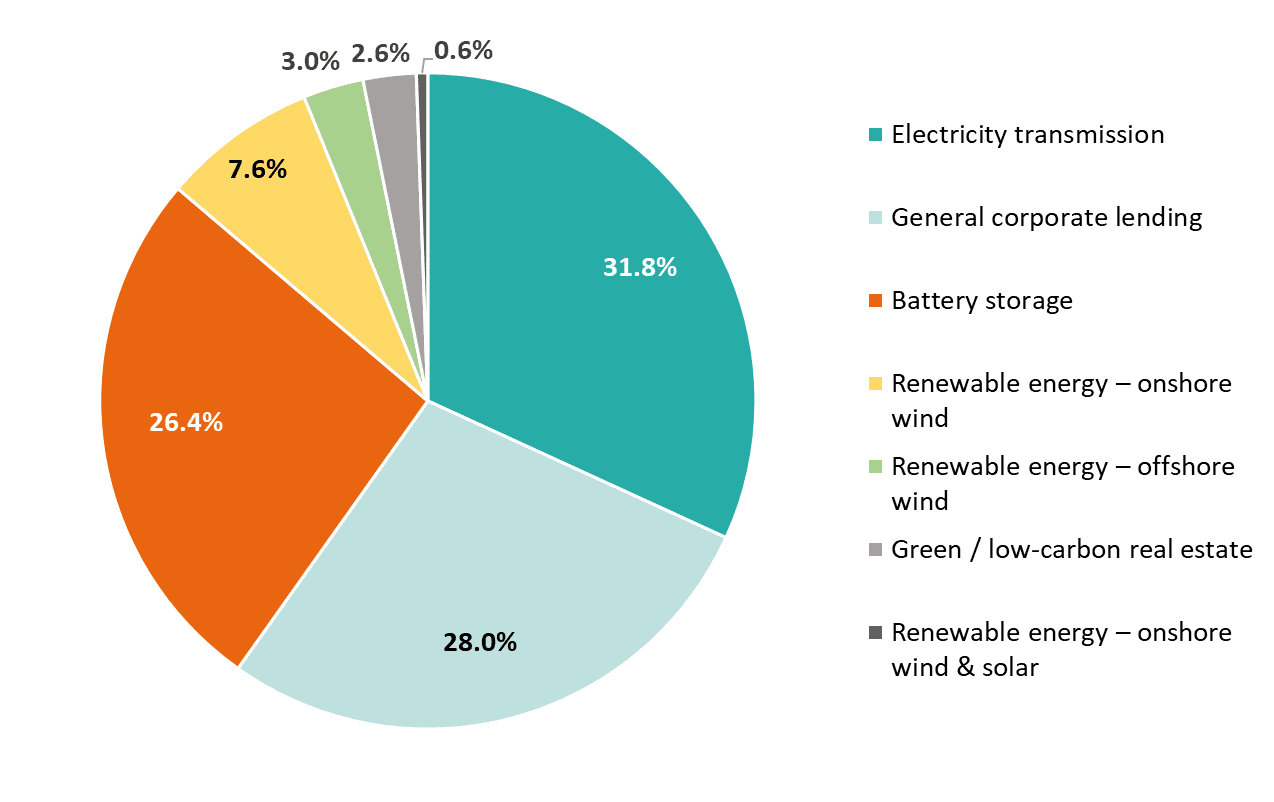

To understand where the deal amounts discussed above have been invested, we analysed the sector allocation of the identified transactions. To do this, we used sector classifications derived from a combination of the Refinitiv Business Classification (TRBC) business sector field and the “use of proceeds” field for each deal, both from LSEG, and supplementary desk-based research to narrow down specific sub-sectors. This was necessary because the dataset does not directly record whether a deal is located in Scotland, requiring us to verify this manually using project-level details. Figure 3 and Figure 4 show the deal total amount disaggregated by sector. We analyse the deals that are partially located (Figure 3) and fully located in Scotland (Figure 4) separately. Table 2 and Table 3 report the same statistics disaggregated by sector and year.

Among the projects partly located in Scotland, renewable wind energy dominates the debt, bonds and equity investments made, representing 42.6% of the total value. This was around £1.8 billion out of £4.3 billion, from the 10 deals spread over 2022 to 2025. The electricity transmission sector attracted the second largest investment total (32%), but this was concentrated in a single large-scale deal. This likely reflects that many Scottish wind projects comprise parts of larger UK-wide or international portfolios. In offshore wind especially, the project company and investors are often headquartered outside Scotland, while the physical asset may sit off the Scottish coast. For deals that are only partly located in Scotland (

Figure 3), the reported deal amounts reflect the total value of the larger, international or UK‑wide transaction, rather than the share corresponding to Scottish assets.

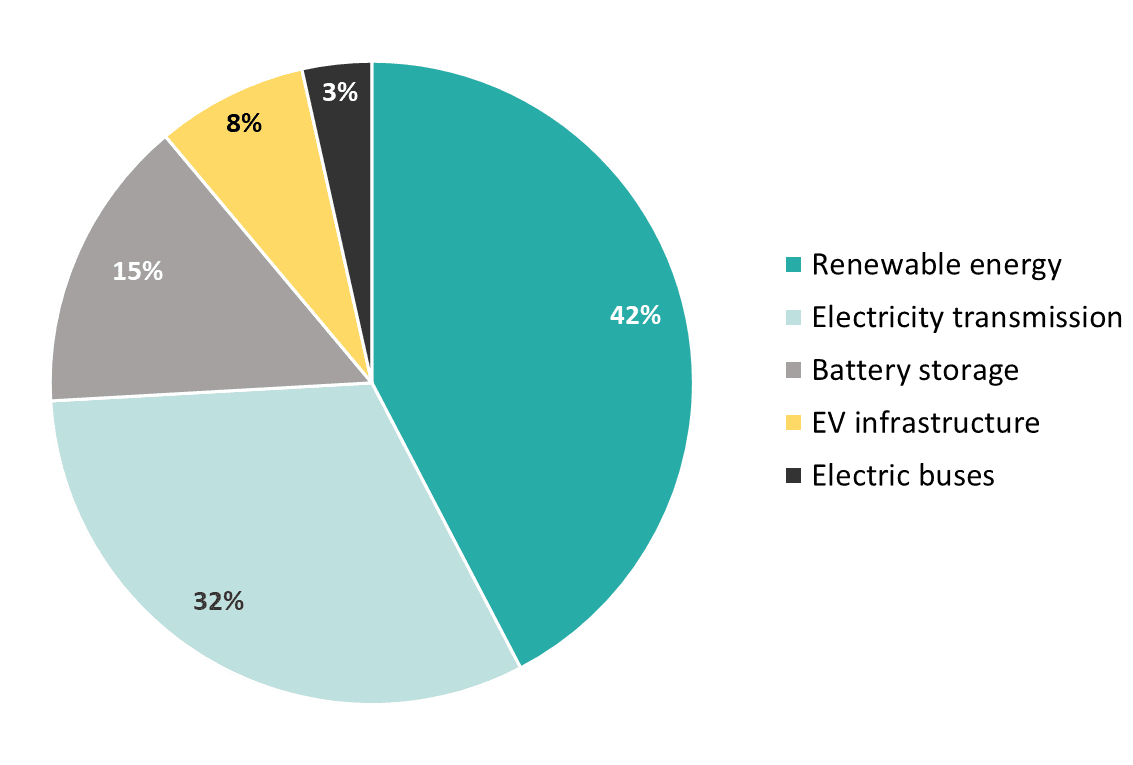

In terms of the projects fully located in Scotland, the largest amounts of investment were directed toward electricity transmission which was 32% of the total investment via three large-scale deals – and battery storage (26%) (Figure 4). High-value electricity transmission projects related to: (i) investment in upgrading grid infrastructure, (ii) improving connectivity and (iii) enabling the transport of renewable energy. One deal related to green/low-carbon real estate has been recorded in 2026 to date.

The dominance of energy sub-sectors in the identified investments is in line with the findings of a CBI Economics study analysing the Scottish net zero economy in 2025. According to their market analysis, the net zero transition has been the most visible in the energy sector in Scotland. A key factor behind this is Scotland’s historic strength in the oil and gas, offshore engineering and subsea capability sectors. These skills and expertise from the traditional fossil fuel sector can be applied in the development of offshore wind, green hydrogen and CCS technologies (CBI Economics, 2026).

Figure 3. Deals partly located in Scotland – percentage of the total amount per sector, 2020-2026 – debt, bonds, equity

Source: LSEG databases, desk-based research.

Figure 4. Deals fully located in Scotland – percentage of the total amount per sector, 2020-2026 – loans, bonds, equity

Figure 4. Deals fully located in Scotland – percentage of the total amount per sector, 2020-2026 – loans, bonds, equity

Source: LSEG databases, desk-based research.

Table 2: Sum of deal amount per sector by year for projects partly located in Scotland

Total and breakdown per sector and year | ||

|---|---|---|

Sector | (GBP, Million) | Number of Deals |

TOTAL – Battery storage | 635 | 3 |

2023 | 175 | 1 |

2025 | 460 | 2 |

TOTAL – Electric buses | 150 | 1 |

2024 | 150 | 1 |

TOTAL – Electricity transmission | 1,363 | 1 |

2025 | 1,363 | 1 |

TOTAL – EV infrastructure | 326 | 1 |

2022 | 326 | 1 |

TOTAL – Renewable Energy (Wind) | 1,817 | 4 |

2022 | 551 | 1 |

2023 | 760 | 2 |

2025 | 506 | 1 |

AGGREGATE TOTAL | 4,292 | 10 |

Source: LSEG databases, desk-based research.

Table 3: Sum of deal amount per sector by year for projects fully located in Scotland

Sector | Total and breakdown per sector and by year | |

|---|---|---|

(GBP, million) | Number of deals | |

TOTAL – Battery storage | 1,362 | 4 |

2023 | 281 | 1 |

2025 | 1,081 | 3 |

TOTAL – Electricity transmission | 1,643 | 2 |

2025 | 1,643 | 2 |

TOTAL – Green / low‑carbon real estate | 135 | 1 |

2026 | 135 | 1 |

TOTAL – General corporate Lending | 1,444 | 3 |

2021 | 500 | 1 |

2023 | 450 | 1 |

2024 | 494 | 1 |

TOTAL – Peatland restoration / carbon‑offset projects | NA | 1 |

2024 | 0 | 1 |

TOTAL – Renewable Energy – Offshore Wind | 154 | 2 |

2024 | 56 | 1 |

2025 | 98 | 1 |

TOTAL – Renewable Energy – Onshore Wind | 394 | 4 |

2022 | 132 | 1 |

2023 | 190 | 1 |

2025 | 62 | 1 |

2026 | 10 | 1 |

TOTAL – Renewable Energy – Onshore Wind & Solar | 29 | 1 |

2025 | 29 | 1 |

TOTAL | 5,161 | 18 |

Source: LSEG databases, desk-based research. Note: The three corporate lending deals in this table fall under the Basic Materials and Utilities sectors; no further sector detail is available for these transactions.

Although the total deal value for the peatland restoration project is not publicly disclosed, the landscape-scale nature of the programme, covering 400,000 hectares across Caithness and Sutherland and involving multiple public and private funding streams, suggests a substantial investment value.

Deals partly located in Scotland are characterised by larger deal sizes and are mainly led by larger energy companies, financial institutions and major banks. Their dominance suggests that Scotland’s green finance landscape is concentrated among a limited number of larger, established players. In terms of deal values by sector, electricity transmission deals were in the range of £1-1.3 billion per deal, whilst renewable energy deals were approximately £500–£650 million per deal, both attracting substantial capital. Meanwhile, battery storage, EV infrastructure deals and electric bus financing tend to be smaller in size at around £150 million per deal and typically funded by commercial banks. No detailed information was available on these deals.

Investments fully located in Scotland involve a broader mix of investors and more variation in deal size across sectors. Electricity transmission deals range from around £500 million to £1 billion per deal and are typically backed by a combination of energy companies, public financial institutions and institutional investors buying green bonds, such as pension funds and insurance companies. Renewable energy deals – which include onshore and offshore wind – range from around £50 million to more than £200 million per deal. They are mainly financed through project-specific funding from commercial banks, infrastructure funds, and sometimes public co-investors, e.g. the Scottish National Investment Bank. Battery storage sits in the mid-range, around £60 million to £280 million per deal, with specialist energy investors and banks playing a key role. These patterns may also reflect differences in risk appetite. For example, a commercial bank can typically take on more risk, versus deals in more mature technologies where asset owners may take on more of a role.

Smaller sectors indicate more variety in investor types. For example, “green real estate”, involves properties with low‑carbon design and operations. One example identified involved transforming a major office site in Edinburgh into 282,000 square foot of sustainable high-efficiency office space. These were typically over £100 million per deal and were usually financed by commercial banks through green debt. Nature-based solutions, such as peatland restoration, tend to be much smaller and rely on a mix of public bodies, e.g. NatureScot, private investors and environmental funding schemes. Peatland restoration initiatives are also supported through public-private programmes like the Flow Country Green Finance Initiative.

Around 28% of investment flagged as sustainable in LSEG, is classified as “general corporate lending”. For these investments it was not specified whether the use of proceeds is for specific projects or general activities. Other sectors such as low carbon and green real estate received smaller shares of investment (see Appendix B for definitions).

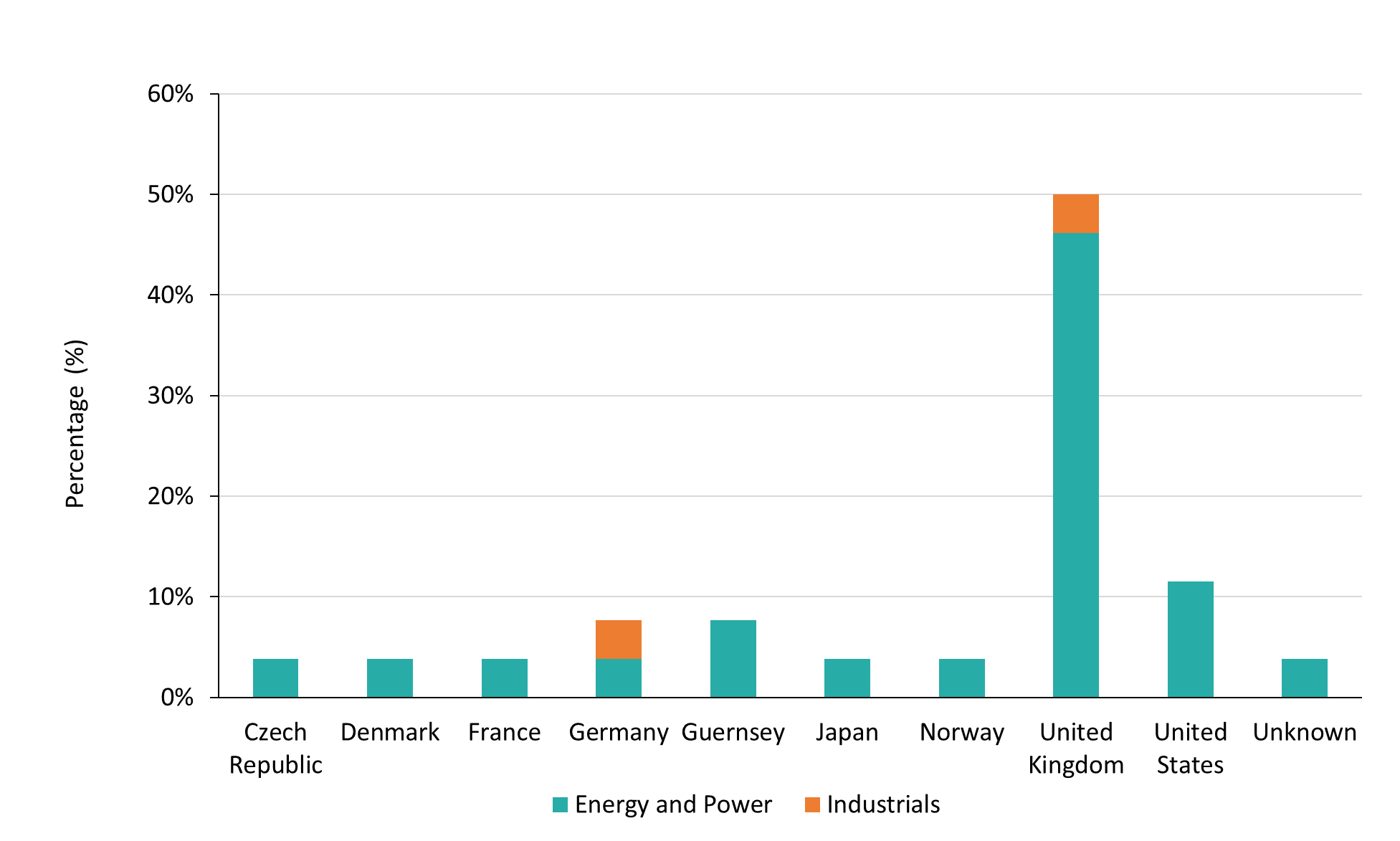

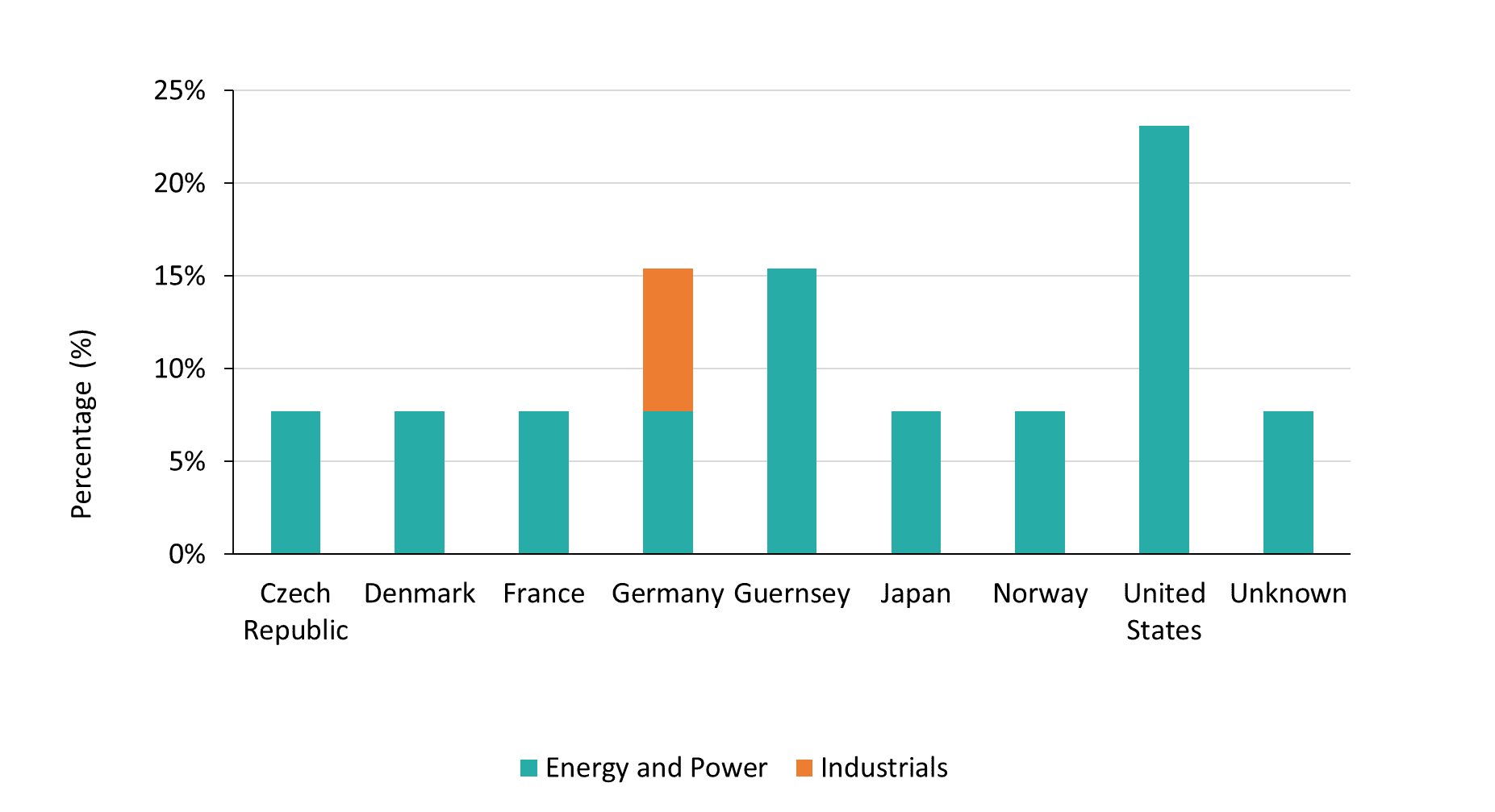

M&A deals were dominated by activity in the energy and power sector this includes offshore wind, onshore wind, solar and hydro company acquisitions (e.g. the Dalquhandy Wind Farm and Beatrice Offshore Windfarm). The nationality and sector of M&A deals are shown in Figure 5 and Figure 6. The investor base was more geographically diverse, with acquirers split relatively evenly between UK-based investors (52%) and international investors from countries including Germany, the US, Denmark and Japan.

The above trends were consistent with the interviewees’ experiences. They noted that investment activity in renewables and green infrastructure in Scotland had been concentrated in more established sectors, particularly off- and onshore wind, hydro and increasingly grid infrastructure and storage. Multiple interviewees noted offshore wind as the dominant area of capital deployment but commented on growing interest in enabling infrastructure such as transmission networks and battery storage (source – interviews with two banks, an asset manager (private markets), and a trade association). They identified a notable gap in areas such as hydrogen and nature-based solutions, where uncertainty around revenue models and market structures was perceived to have constrained investment appetite (source – interviews with an asset manager in public markets, and an asset manager in private markets). Similarly, they considered some noted retrofit and energy efficiency in the built environment had struggled to scale due to weak end-user demand and a lack of compelling financing propositions (source – interviews with two banks).

Figure 5. Cross-border and intra-border M&A deals in Scotland, 2020-2026, including UK

Figure 6. Cross-border and intra-border M&A deals in Scotland, 2020-2026, excluding UK

Source: LSEG databases, desk-based research

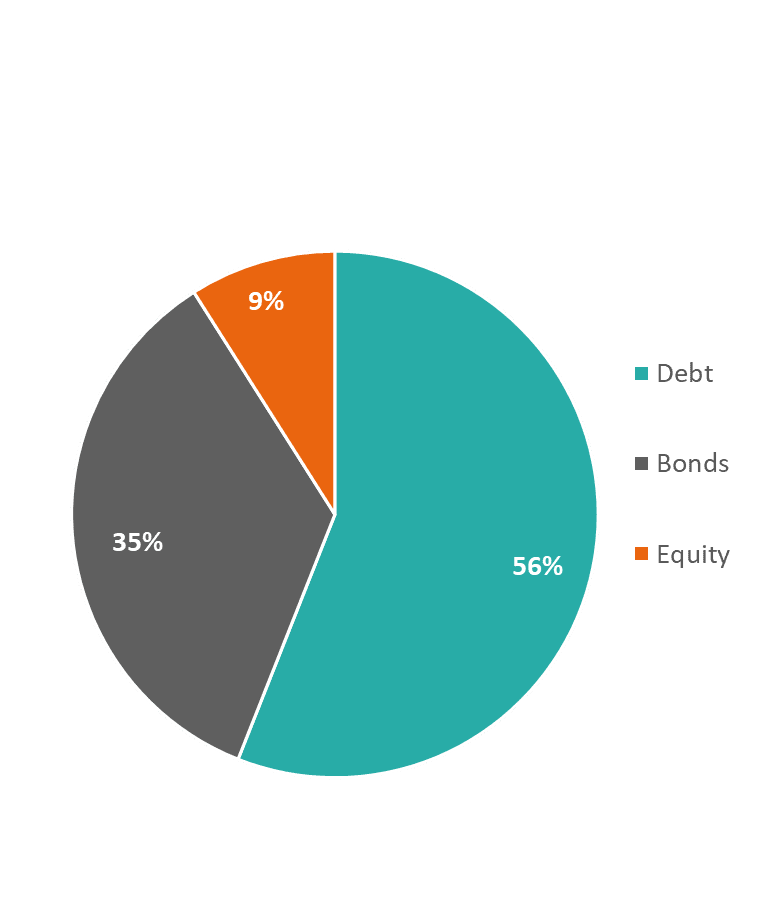

Financing structures and instruments

Loans were the primary financing instrument, accounting for 56% of the total deal amount. As above, the deals in this section were identified through LSEG’s deals database which captures publicly disclosed financing deals. This financing was predominantly directed towards large-scale renewable energy generation, battery energy storage systems (BESS) and electricity network upgrades. The majority of these deals take the form of term loans and revolving credit facilities tied to a specific green project rather than corporate lending backed by the company balance sheet. Bridge short-term loans and other corporate loan structures account for only three deals, all of which are partly located in Scotland (refer to Table 7 in Appendix A for more detail on the deal categories’ breakdown).

Bonds account for 35% of the total deal amount and are commonly used to finance projects fully located in Scotland, including Euro-medium term notes and retail crowdfunding bonds. They were used to support large-scale renewables, transmission upgrades in northern Scotland, and for general corporate purposes, such as refinancing corporate debt.

Equity-based deals appear to play a minor part in financing the green transition to date, representing 9% of total deal value. They largely comprise early-stage or blended public-private investments, typically the highest-risk but potentially highest-reward transactions in the investment cycle. An example is the Scottish RenewCo £38 million funding, in which both public sector bodies, including the Scottish National Investment Bank, and private investors provided capital to advance a 7GW onshore wind and solar pipeline (ESG News, 2025).

Other equity investments funded environmental restoration projects such as Flow Country peatlands and BESS projects. These supported grid preparation, carbon sequestration, biodiversity and grid stability. The concentration of equity activity in early-stage and blended structures points to a critical juncture in Scotland’s green finance landscape. Where revenue certainty is insufficient to attract debt financing and the risk profile remains too high for conventional lenders, public and mission-driven investors such as the Scottish National Investment Bank and the National Wealth Fund play a key role in absorbing first-loss risk and unlocking subsequent private investment.

The distribution of financing instruments used for green investment is shown in Figure 7. These data are calculated based on the total monetary value of each deal. For a more detailed breakdown see Table 7 in Appendix A.

Figure 7. Shares of the instrument types used in green investments in Scotland based on total monetary value, 2020-2026

Source: LSEG databases.

Interviewees confirmed that financing structures have largely remained conventional. They tend to rely on a mix of balance sheet lending and project finance structures such as a special purpose vehicle (SPV) with equity and senior debt. They also noted the increasing integration of ESG criteria into credit assessments (source – interviews with a bank and an asset manager in private markets). Banks primarily provide traditional lending products, including green loans. Larger infrastructure investors deploy equity through project finance vehicles, direct equity stakes, co-investments and secondary market acquisitions of operational assets, particularly in large-scale infrastructure (source – interviews with a bank, asset manager (private markets), and an asset owner). Investment sizes vary significantly, ranging from lending to SMEs below £1.5 million, to large-scale infrastructure projects exceeding £500 million. A substantial proportion of activity occurs in the secondary market, focused on de-risked, income-generating assets (source – interviews with a bank, and two asset managers (private markets).

The main financing approaches identified were:

- Balance sheet lending and green loans: banks primarily provide traditional lending products, including green debt, to businesses ranging from SMEs (below £1.5 million) to large corporates.

- Project finance via Special Purpose Vehicles (SPVs): entities that combine equity and senior debt for a single project, typically operating under a head contract with a local authority and subcontracting to a Tier 1 contractor, which helps allocate risk clearly.

- Direct equity and co-investment: larger infrastructure investors deploying equity through direct stakes, co-investments and secondary market acquisitions of operational assets, particularly in large-scale infrastructure (source – interviews with a bank, asset manager (private markets), and an asset owner).

- Secondary market: a substantial proportion of activity involves buying and selling existing operational assets rather than financing new ones, reflecting investors’ preference for de-risked, income-generating projects (source – interviews with a bank, and two asset managers (private markets).

- The increasing integration of ESG criteria into credit assessments was also noted (source – interviews with a bank and an asset manager in private markets).

Asset classes

An asset class is defined as a group of investments that have similar attributes, behave similarly in the market, and are subject to the same regulations (A. Ganti, 2025) (see Appendix B for a full list). This section examines the types of assets related to the investments described above, i.e. the main investment categories in which finance was invested.

To provide additional insight into investment patterns, transactions were analysed from two asset-class perspectives. The first considers the type of investment exposure represented by the transaction, such as private equity, private debt or fixed income. The second considers the underlying assets or activities targeted by the investment, such as infrastructure or natural capital. These are represented in the ‘Asset class’ and ‘Asset class subcategory’ columns of Table 4, respectively. Given differences between the financing and M&A datasets used for the analysis, the classification approach varied slightly between them. For financing transactions, the underlying asset class was identified based on the stated use of proceeds, while for M&A transactions, it was determined based on the characteristics of the acquired company or asset.

Across all deals, excluding M&A transactions, private debt was the most common (61% of transactions), followed by fixed income instruments (31%) (see Table 4 below). Private equity transactions accounted for only 8% of deals. Within private debt, infrastructure debt was the prevailing subcategory (50 percentage points (p.p.)), followed by corporate debt (8 p.p.) and real estate debt (3 p.p.). Green bonds accounted for all fixed income transactions. For private equity, the subcategories were growth equity (6 p.p.) and natural capital investment (3 p.p.). Overall, debt-based instruments played a central role in green investment activity during the period analysed.

In our sample, there was a high degree of concentration in infrastructure-related investments, which was not only due to the prevalence of infrastructure debt transactions. Infrastructure assets were also financed through fixed-income and equity transactions, potentially indicating an investor preference for assets with established development pathways and long-term revenue potential. This composition of investment activity has remained relatively stable over the period analysed. While the number and value of transactions have increased, this growth was largely concentrated within existing asset classes. Infrastructure has continued to account for the majority of identified investments. This is partly explained by this research solely investigating deals over £10 million.

The representation of other asset classes, such as investments in natural capital (via private equity) and in green real estate (via private debt), was limited. The small number of transactions may indicate that these markets are less mature. Alternatively, this may be due to such deals financed through channels not captured in this analysis, and/or data not being in the public domain.

Table 4: Asset class types of the completed deals, 2021-Feb 2026

Asset class | Number of investments | Asset class subcategory |

1. Private debt (total) | 22 | Real assets (infrastructure) |

Infrastructure debt | 18 | |

Corporate debt | 3 | |

Real estate debt | 1 | |

2. Fixed income (total) | 11 | Real assets (infrastructure) |

Green bonds | 11 | |

3. Private equity (total) | 3 | |

Growth equity | 2 | Real assets (infrastructure) |

Natural capital investment | 1 | Real assets (natural capital) |

Source: LSEG, desk-based research

The asset class used for M&A activity was less concentrated in infrastructure assets than other deals and included investment in a broad range of green sectors. While the majority of acquisitions still involved companies with exposure to infrastructure assets, many transactions targeted project developers, engineering firms, consultancies, technology providers and other specialised service businesses. As a result, it was not always possible to identify an underlying asset class, especially where the target company’s activities were the provision of services. Overall, M&A activity has facilitated investment in infrastructure assets and supported investment in technical capabilities, development expertise, and specialised services required to deliver the energy transition. Acquisitions have been used not only to obtain ownership of low-carbon assets, but also to strengthen capabilities across the wider green economy value chain. Where data were available, companies were mainly acquired through private equity.

Other investment characteristics

Investors in Scottish renewable and green infrastructure projects were mainly developers or operational firms, headquartered in Scotland or elsewhere in the UK. Operational firms describe those that are neither holding companies nor special purpose vehicles (SPVs), which applies to most corporations in the LSEG dataset. Examples include Pulse Clean Energy Ltd and FirstGroup PLC, whose primary function is to provide a service or good. Our data indicates that most investors were limited companies (65%), with public limited companies accounting for 15%. The remaining 20% are non-company entities such as public authorities. Of the investors from outside of the UK, a small share was from the rest of Europe (7.14%, from Finland and Denmark for example), while 10.7% of deals are from Canada and the United States.

Most deals financed with private capital were in the large-scale offshore wind and battery storage sectors. Public entities participated in strategic, community or blended-finance deals (e.g. Flow Country peatland restoration (discussed in Case Study 2), Orkney community wind and the Caithness-Moray HVDC connection). Debt was used equally by private and public investors. Public entities tend to play a larger role in bond financing, while equity is more commonly provided by private investors or blended capital.

Private investors and corporate subsidiaries were prevalent in M&A activity in Scotland’s renewable energy sector, with publicly listed companies playing a smaller but notable role. A total of 12 deals (48%) involved private investors. Of these, 8 (32%) were subsidiaries of larger groups and 5 (20%) were publicly listed companies, often using SPVs which are common in energy infrastructure deals. While it is not possible to confirm the specific characteristics of these SPVs based on publicly available information, SPVs are typically structured as project-specific entities.

Conditions influencing investment decisions

This section evaluates evidence on the factors influencing investor confidence in Scottish renewable and infrastructure projects. As such, it draws on eight interviews, and a written response from one institution. Where relevant, we also refer to published research to triangulate these views. As the sample size is not statistically representative, the input gathered does not provide a robust reflection of the views of all market participants.

Policy transparency and regulatory stability were perceived as key determinants of investor confidence. Respondents emphasised the importance of a stable legal and regulatory environment, particularly in established sectors such as offshore wind. In these, Scotland was seen to benefit from mature contracting frameworks and predictable governance conditions (source – interviews with a bank and an asset manager (private markets). However, with emerging sectors such as hydrogen, battery storage or nature-based solutions, some interviewees suggest a lack of familiarity and certainty around policy and longer decision processes may have impacted investor confidence (source – interviews with two asset managers (public and private markets), and a trade association). Stakeholders (asset managers, private markets) noted the absence of long-term revenue guarantees for hydrogen projects and limited visibility of local authority pipelines for early-stage renewable energy initiatives. Other research notes the policy landscape is still considered by some to be complex and cumbersome for many green sectors, including building retrofitting and electricity grids (GEFI, 2024a).

Revenue certainty emerged as a critical factor influencing investment decisions, particularly for capital-intensive infrastructure. Projects offering long-term income streams or supported by government appeared to be viewed by interviewees as significantly more attractive to institutional investors (source – interviews with an asset manager (private markets) and an asset owner). These included pension funds seeking stable, long-duration returns (source – interviews with an asset manager (private markets) and a trade association). This involvement was especially important in reducing perceived risk and enabling investment in large-scale assets once key development milestones, such as land access, had been secured (source – interviews with a bank and an asset manager (private markets). One interviewee noted that large infrastructure projects lasting 25 years or more require confidence in a minimum return (source – interview with an asset manager (private markets). The predictability of revenue streams is also important to debt lenders, who require confidence in a project’s cash flows before committing financing.

Interviewees from two banks indicated that their offering of green lending, for green residential real estate, was primarily demand-led, suggesting that capital availability was not the primary constraint where viable opportunities existed (source – interviews with two banks). This aligns with findings from the Scottish Government’s Green Heat Finance Taskforce that private lenders are doing significant work to develop and test products such as green mortgages. It noted the importance of wider measures in creating the overall conditions required for this market to flourish, with demand stimulation being a critical factor (Green Heat Finance Taskforce, 2023). These conditions include regulation, quality assurance standards, a well skilled and knowledge supply chain, and clear consumer protection measures. In relation to capital allocation more broadly, a private markets asset manager noted there is no internal cap or limit on capital allocation in Scotland, with investment decisions driven entirely by the availability of suitable opportunities (source – interview with an asset manager (private markets).

Several structural and delivery-related barriers were identified by interviewees as constraining investment. These included the lack of visible project pipelines and grid-related challenges, which affected project timelines (source – interviews with a bank and a trade association). A lack of a visible pipeline may make it difficult for investors to commit capital in advance or plan resource allocation. While some stakeholders noted the lack of a visible investment pipeline, it was not clear whether this was due to the low number of projects or a transparency issue. Other research has found that when major projects were known to investors, they were focused on a relatively small number of sectors, which meant little opportunity to diversify risk (Investor Panel, 2023).

Given the above, the Scottish Government has published a pipeline of costed and prioritised projects. The Green Investment Portfolio was launched in 2020 comprising ten market-ready projects with the value of £1.16 billion (Scottish Government, 2020). Interviews with stakeholders suggested mixed levels of awareness of the initiative. Further work is currently underway by the Scottish Government to raise awareness and publicise these portals and pipelines as part of its approach to investment.

Additionally, insufficient grid capacity may create uncertainty on whether it will be possible to integrate new RES projects in the energy system. In addition, concerns over weakening public support for decarbonisation and broader sensitivities around energy costs were noted as factors influencing the policy and investment environment (source – interviews with a bank and an asset manager (public markets). These factors may also complicate long-term commitments for investors, increasing the risks and affecting the revenue model.

Challenges were perceived as more acute for projects in emerging or less mature sectors. Hydrogen and nature-based solutions were consistently identified as facing difficulties in securing finance due to uncertain market structures and a lack of clear, reliable revenue streams (source – interviews with two asset managers (public and private markets). Respondents also highlighted the importance of mechanisms such as public guarantees, blended finance and long-term revenue support in enabling investment in these higher-risk areas, where purely commercial financing remained difficult to obtain (source – interviews with a bank, and two asset managers (public and private markets).

Other factors influencing investment decisions were mentioned less frequently but remain relevant. These included specific regulatory constraints such as high charges affecting certain technologies (e.g. pumped storage), as well as the importance of clear pathways for scaling projects from early-stage development to bankable infrastructure (source – interview with a bank and an asset manager (private markets)).

Investment in Scotland’s green and renewable sector is largely driven by existing project opportunities, as well as policy transparency, regulatory stability and revenue certainty. Structural and delivery-related barriers remain, particularly for emerging sectors such as hydrogen and nature-based solutions. While less frequent, other factors such as investor preferences and project scale also influence decision-making, highlighting the need for a stable and supportive environment to sustain growth in green investment.

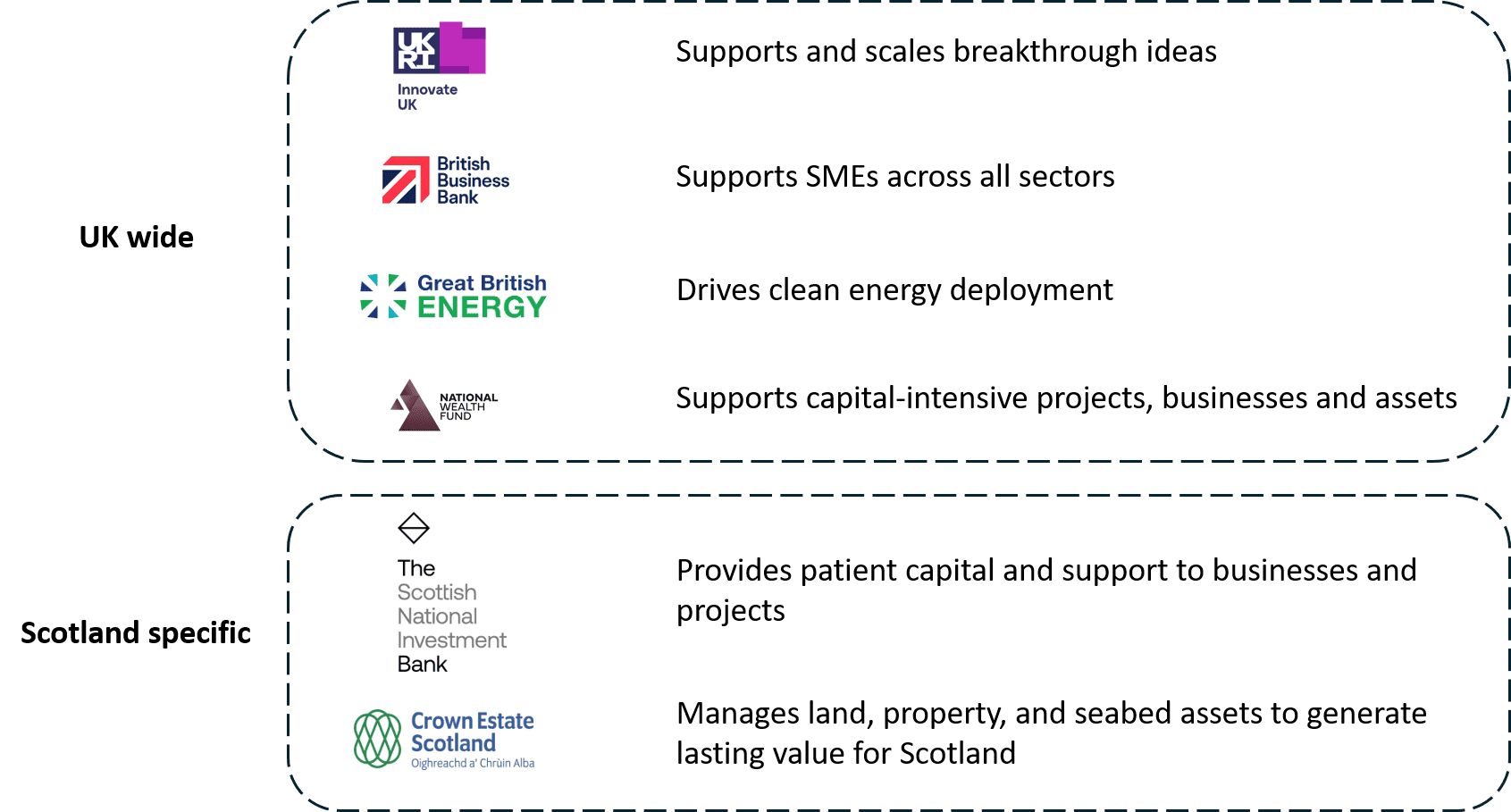

Public financial institutions

Public financial institutions (PuFins) play complementary roles in crowding in private finance in Scotland. These include the Scottish National Investment Bank, the British Business Bank, the National Wealth Fund, British Patient Capital, Innovate UK, and GB Energy. There are also other public institutions and companies investing or supporting mobilisation of finance in Scotland, such as Scottish Enterprise and Scottish Futures Trust. Each target specific market failures and investment challenges and operates in different sectors based on technology and market maturity. These include: emerging innovations (Innovate UK, British Business Bank); supporting businesses at the growth stage (British Business Bank, GB Energy, National Wealth Fund); to supporting mature markets (British Business Bank, GB Energy, National Wealth Fund) as set out in Figure 8 below (HM Government, 2025).

The Scottish National Investment Bank (SNIB) provides patient capital, while seeking commercial, societal and environmental impacts from its investments. It invests in debt, equity and external funds (Scottish National Investment Bank, 2025). Since its launch in 2020, SNIB has invested £348.5 million and mobilised an additional £1 billion of third-party capital in net zero-related investment opportunities, which accounts for the largest share of its portfolio. These investments are in addition to the volumes described in the previous section, which were sourced from databases, apart from one £29 million deal. Priority sectors for the Bank’s net zero mission are battery and storage technologies, industrial decarbonisation, grid infrastructure, circular business models and materials, natural resources, and offshore wind supply chain and technologies. Relevant housing sectors from the Bank’s place mission include affordable and sustainable mixed tenure housing and decarbonisation at scale (The Scottish National Investment Bank, 2025). In 2024, SNIB held 39 investments, of which 16 deals were in net zero sectors, including renewable energy, energy infrastructure equipment, and alternative fuels. Leverage of private capital has been highest for investments in green sectors (The Scottish National Investment Bank, 2025). The case study in Box 1 below outlines a key project with SNIB involvement. Further case studies addressing projects with different characteristics in different sectors are summarised in Appendix D.

Meanwhile, the British Business Bank and Innovate UK support smaller early stage businesses. The British Business Bank provides loans and debt finance, including to smaller businesses. The Bank acts as a first mover and tends to invest in riskier but innovative businesses. Similarly, Innovate UK finances innovative businesses at the earliest stage, offering flexible finance and patient capital (HM Government, 2025). Innovate UK provides grants and loans, as well as advisory support for accessing business networks, regular engagement, and technology due diligence (British Business Bank, n.d.; Innovate UK, n.d., 2025).

The National Wealth Fund (NWF) invests for the longer-term. While its risk appetite is greater than that of commercial banks, the Fund focuses on technologies at later stages of development, construction, and commercialisation (HM Government, 2025). Clean energy, CCUS, hydrogen, battery manufacturing and EV supply chain, green steel, power grids, and energy storage are among the priority sectors (National Wealth Fund, n.d.). Additionally, the fund plans to target sustainable aviation fuels and critical minerals, and to accelerate the delivery of core infrastructure, including offshore wind, solar, building retrofitting, heat networks, and EV charging. NWF provides loans, equity and guarantees. In Scotland, it has invested £1.6 billion to upgrade the national grid and enable clean power and energy security across the UK. It also provides bespoke project development and investment support to the local government (National Wealth Fund, n.d.).

Some of the PuFins also partner to crowd in private finance. For example, GB Energy, NWF and SNIB invested in the Pentland Floating Offshore Wind Farm in Scotland, which was developed by funds managed by Copenhagen Infrastructure Partners (NWF, 2025). SNIB and NWF also jointly invested in Nova Innovation to scale up production of recyclable and compostable packaging (HM Government, 2025).

PuFins also support community projects in green sectors. In 2025, GB Energy (GBE) pledged to provide finance for local renewable energy projects in Scotland. Scottish Government has already defined a list of projects to be supported, including by its own investment (UK Government, 2025a). This commitment is part of GBE’s Local Power Plan, under which up to £1 billion of public investment is planned to scale community and locally owned energy projects across the UK (DESNZ, 2026). The plan provides for direct funding through grants, debt, and project finance, aiming to unlock wider investment in local and community energy projects. GBE has also established a £5 million Community Fund to support energy projects, though it is currently limited to England. It invests in equity and joint ventures for both clean energy projects and supply chain investments. It also provides grants, loans, blended finance, and capacity support for local government or community groups with a ringfenced Scottish element (HM Government, 2025).

Some public agencies facilitate increasing private investment in green sectors. For example, Crown Estate Scotland (CES) contributes to the development of offshore wind in Scotland by awarding and managing leases and other enabling work (Crown Estate Scotland, n.d.). It deploys patient capital, aiming to create environmental or social value alongside commercial returns. The Crown Estate – a separate entity to CES – focusses on a broader list of sectors such as science and innovation, clean energy, and nature and biodiversity (HM Government, 2025).

Overall, public financial institutions play a key role in addressing market gaps and enabling investment across different stages of the financing lifecycle. In doing so, they help to reduce risks and support the mobilisation of private capital into green sectors in Scotland. The ecosystem of PuFins with diverse mandates and risk appetites helps create financing continuity for businesses in green sectors as they transition from innovation and demonstration to commercial deployment. An important contribution is the provision of patient capital. This is particularly important in green sectors, which face long payback periods, often greater policy uncertainty, and substantial upfront infrastructure costs. In these cases, commercial finance alone may be reluctant to invest at early stages.

There was limited evidence from interviewees on the role of public institutions in mobilising private finance. However, stakeholders stressed the importance of a favourable regulatory environment and support mechanisms for the green sectors. The effectiveness of public finance institutions in mobilising private capital depends not only on the availability of public investment, but also on wider policy and regulatory certainty across the UK, particularly in capital-intensive and technologically nascent sectors.

Figure 8: Map of public financial institutions relevant for Scotland

Source: An introduction to the UK public investment landscape, HM Government.

Box 1. Case study: Quanterness Wind Farm loan

The Quanterness wind farm is a 28.8 MW community-owned onshore project in the St Ola region of the Orkney Islands, developed by Orkney Islands Council with financial support from the National Wealth Fund. Approved for investment in 2025, the project forms part of a wider portfolio of community wind developments across the islands. It will consist of six turbines, each with a capacity of 4.8 MW, and has an estimated build cost of £50 million. The project is fully financed through a £62.1 million government loan provided by the NWF, offering favourable interest rates aligned with government bond yields. A 15-year Contract for Difference (CfD) has been secured, ensuring long-term revenue stability and strengthening the project’s financial viability. Construction is expected to begin in 2027, with operations commencing in 2028, and debt repayment planned largely within the CfD period.

The investment is an example of broader policy support for onshore wind capacity in the UK and Scotland, as well as of the efforts to enhance local community benefits from RES projects. Quanterness benefits from proven wind technology, high local wind resource, and the potential to export electricity to the Scottish mainland via a planned interconnector. The project is expected to generate approximately 96.6 GWh of electricity annually – enough to power around 26,000 households – while avoiding approximately 40,000 tonnes of CO₂-eq each year. The project illustrates the role of public financing and revenue stabilisation mechanisms for development of green sectors.

Future investment appetite and priorities

Introduction

As noted in section 3.1, the Scottish government is developing a supportive environment to attract investors towards sustainable finance opportunities. In line with actions originally set out in the Green Industrial Strategy (2024), the government hosted a Global Offshore Wind Investment Forum in 2025, where it highlighted £500 million of investment in the Scottish offshore wind supply chain and outlined a goal of leveraging £1.5 billion of private investment.

The InvestScotland portal, also launched in 2025, is hosted by Scottish Development International, the agency responsible for trade and inward investment as the international arm of Scottish Enterprise. It showcases large-scale investment opportunities in renewable energy and other infrastructure. It is intended to support participation from international investors in major projects already underway or planned. These projects include Orkney energy infrastructure, Green Volt Floating Offshore Wind Farm, and Coire Glas pumped storage hydro.

This section provides an overview of publicly available information on which financial institutions are looking to meaningfully, structurally invest in Scottish projects in the short and medium-term. We focussed on the companies identified in Section 4 with completed deals in Scotland since 2020 and the major financial services firms currently operating in Scotland. Furthermore, we conducted a review of relevant news portals to identify published investor plans in Scotland since 2020. We also asked investors active in Scotland to comment on their investment plans. These stakeholders include large UK-based retail and commercial banks, globally active asset managers (across private and public markets), and infrastructure investors. Data in this section should not be treated as exhaustive. A lack of data on certain sectors does not imply a lack of investor interest. Evidence from stakeholders was used to complement desk-based research. Appendix A provides more details on the specific methodology. It should be noted that while the analysis of past deals in Section 4 does not include balance sheet financing, this form of financing is included in the analysis of future plans. This reflects the data available in public sources.

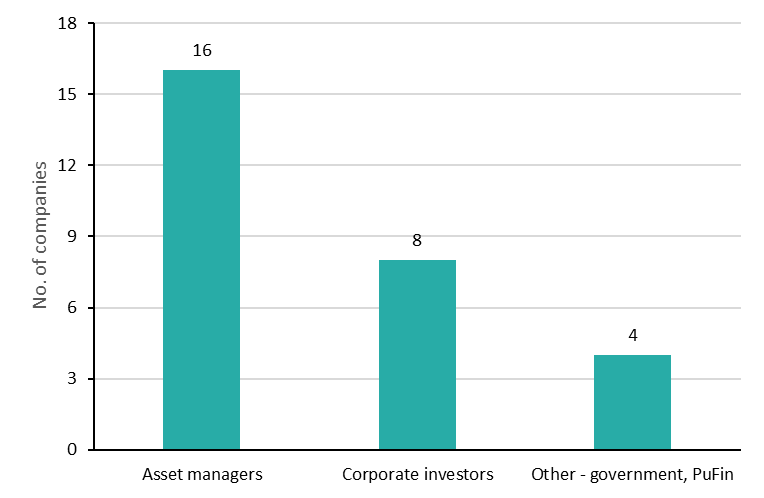

Institutions planning to invest in Scotland

A total of 28 existing and new investors has announced plans to invest in green sectors in Scotland. Of these, 16 were asset management companies, eight were corporate investors, and four were PuFins (see Figure 9). The asset management category includes those seeking to adopt several different investment strategies, including private equity strategies, such as venture capital and growth equity (see Appendix B for definitions), and infrastructure investing.