Scotland’s businesses, infrastructure, communities and natural environment face increasingly severe climate change impacts. Yet, the actions required to adapt to those changes – how they will evolve over time, what they will cost, and who should pay – remain poorly understood.

This report provides the first estimate of Scotland’s climate adaptation investment needs through to 2040 across five sectors:

- agriculture;

- communities (focused on flooding);

- the natural environment (focusing on woodland creation, peatland, nature restoration);

- transport (focusing on trunk roads, motorways, railways); and

- water (focusing on public water and wastewater services).

This work is intended to support the Scottish Government in building an evidence base ahead of the fourth Scottish National Adaptation Plan (SNAP4).

Estimating future adaptation cost is inherently challenging. It requires assumptions about future warming, the level of climate risk that society are willing to tolerate, and the associated scale of adaptation and residual damages. Deep uncertainty in climate projections, socioeconomic change, asset vulnerability, and political priorities make precise modelling both challenging and resource intensive.

As a result, the findings in this report should be treated as pragmatic, evidence-based approximations that indicate the order of magnitude of investment needs—not definitive targets.

Estimated climate adaptation investment need

Adaptation investment needs across the sectors and subsectors assessed in this study are estimated at £7.8–£14.2 billion between 2026 and 2040, or £566–£1,027 million per year.

Previous estimates from the Climate Emergency Response Group, Paul Watkiss Associates, and the Office for Budget Responsibility suggested Scotland’s total adaptation costs would range from £196 million to £1,340 million per year from 2030 onwards. These are based on UK wide analyses and international benchmarks. Sector specific estimates in this study fall within that range. However, because this analysis covers fewer sectors than the Scottish National Adaptation Plan, the findings suggest that Scotland’s full adaptation investment needs may be higher than previously anticipated.

The results in this report carry low confidence and should be viewed as indicative, not precise. The sector-specific figures represent order of magnitude estimates designed to inform policy discussion and future research, rather than definitive costings.

The macroeconomic effects of investing in climate adaptation

This research also looks at macroeconomic modelling to estimate the wider economic effects of similar levels of adaptation spending.

A full assessment of the macroeconomic costs and benefits of adaptation were beyond the scope of the study. However, the study did model the direct economic effects of adaptation spending across sectors. It also explored how different approaches to cost recovery affect economic activity, employment, and household incomes.

The modelling consistently shows that adaptation spending generates a positive economic stimulus during the investment period, supporting jobs and output particularly in construction, engineering, and land-based supply chains. However, the way costs are recovered – whether through income-tax, charges or through public spending cuts – matters considerably.

How will costs be borne by households, businesses, and the public sector?

The researchers made additional analysis of how adaptation costs might be shared between the public and private sectors.

The study investigated how adaptation is currently funded in each of the sectors. Climate adaptation in Scotland is currently funded predominantly by the public sector. However, households and businesses pay more than previously understood, through Council Tax and Non-domestic rates. Households and businesses also bear some costs directly, for example through property-level insurance and on-farm investments, but this remains modest in most sectors.

This balance is unlikely to shift fundamentally. Most of the adaptation investment – including flood protection, transport resilience, and natural flood management – generates little or no direct financial return and is therefore structurally dependent on public funding. Analysis suggests that approximately three-quarters of adaptation investment needs will require public financing regardless of innovations in private finance mechanisms.

Scope to boost private sector participation

The study reviewed the innovative funding and financing models being used internationally and within Scotland. Analysis found that there is modest potential to increase private sector participation in adaptation funding and financing across all five sectors, and a range of innovative mechanisms are emerging. These include parametric insurance in agriculture, biodiversity credits and voluntary carbon markets in the natural environment, green and resilience bonds for flood and transport infrastructure, and catchment co-investment models in water.

Recommendations

The research report includes several recommendations for further research. These include developing adaptation targets and risk tolerance thresholds, strengthening the evidence base for the “triple dividend”, and creating frameworks for prioritising actions that account for rural vulnerability, social equity, and Just Transition principles.

For additional recommendations and details of how the investment estimate where reached, please read the report.

If you require the report in an alternative format, such as a Word document, please contact info@climatexchange.org.uk or 0131 651 4783.

Research completed: March 2026

DOI: https://doi.org/10.7488/era/7087

Executive summary

Background and purpose

Scotland’s businesses, infrastructure, communities and natural environment face increasingly severe climate change impacts. Yet, the required adaptation actions – how they will evolve over time, what they will cost, and who should pay – remain poorly understood.

This report provides the first estimate of Scotland’s climate adaptation investment needs through to 2040 across five sectors (and eight subsectors):

- agriculture;

- communities (flooding);

- the natural environment (woodland creation, peatland, nature restoration);

- transport (trunk roads, motorways, railways); and

- water (public water and wastewater services).

It then presents two further discrete analyses: macroeconomic modelling to estimate the wider economic effects of similar levels of adaptation spending, The five sectors were chosen to reflect the diverse approaches required to assess indicative adaptation costs. We examine four aspects of climate adaptation investment: required investment, its macroeconomic impacts, public-private funding splits, and the potential to mobilise private capital. This work is intended to support the Scottish Government in building an evidence based ahead of the fourth Scottish National Adaptation Plan (SNAP4).

Estimating future adaptation cost is inherently challenging. It requires assumptions about future warming, the level of climate risk that society are willing to tolerate, and the associated scale of adaptation and residual damages. Deep uncertainty in climate projections, socioeconomic change, asset vulnerability, and political priorities make precise modelling both challenging and resource intensive. As a result, the findings in this report should be treated as pragmatic, evidence-based approximations that indicate the order of magnitude of investment needs—not definitive targets.

Why adaptation investment matters

Failing to invest in mitigation and adaptation carries significant economic costs. Estimates for this study suggest climate change could reduce GDP by 0.3-0.4% a year in the 2030s, rising to 1.2-1.6% by the 2050s and 1.6-3.3% by the 2070s. Other studies project higher impacts but these depend on the models and assumptions used. The Scottish Environment Protection Agency estimate that flooding alone already costs Scotland an estimated £500 million per year. Adaptation can reduce these damages, but it also requires upfront investment, is rarely fully effective, and involves trade‑offs between expenditure and residual risk. The key question is therefore not whether to invest in adaptation, but how much and who should pay.

Adaptation investment also delivers wider benefits, often described as the “triple dividend”: avoided losses, economic gains, and social and environmental co-benefits such as biodiversity improvements, carbon sequestration, and better mental health. These co-benefits further strengthen the economic case for adaptation.

Climate costs are projected to rise significantly beyond 2040. The research and strategic priorities below are therefore time-sensitive: early action on adaptation can reduce long-run costs and delivers benefits that delayed investment may not recover.

Estimated climate adaptation investment need for Scotland in five sectors

Adaptation investment needs across the five sectors and eight subsectors assessed in this study are estimated at £7.8–£14.2 billion between 2026 and 2040, or £566–£1,027 million per year. Sector and subsector level results are shown in Table 1.

Previous estimates from the Climate Emergency Response Group, Paul Watkiss Associates, and the Office for Budget Responsibility – based on UK wide analyses and international benchmarks – suggested Scotland’s total adaptation costs would range from £196 million to £1,340 million per year from 2030 onwards. The sector specific estimates in this study fall within that range. However, because this analysis covers fewer sectors than the Scottish National Adaptation Plan, the findings suggest that Scotland’s full adaptation investment needs may be higher than previously anticipated.

The study also compared the estimated annual adaptation investment needs to current allocations in the Scottish budget. It found that only the agriculture sector is likely meeting its adaptation needs. The communities (flooding), transport, and nature sectors will likely require additional investment to maintain current risk levels. We could not assess the water sector due to a lack of available information on existing adaptation spending.

The results in this report carry low confidence and should be viewed as indicative, not precise. Confidence levels vary by sector (Table 1) due to fragmented data, limited understanding of asset vulnerability, and the lack of clear adaptation targets to scale investment needs. Where Scottish specific data was unavailable, we crosschecked estimates with international comparisons, which also have limitations because of differing risks and institutional contexts. These figures therefore represent order of magnitude estimates designed to inform policy discussion and future research, rather than definitive costings.

Table 1: Climate adaptation investment estimates for 14 years 2026/27 to 2039/40 across five sectors and their key sub-sectors (2026/27 prices). Where available, current budget (or estimates) are presented alongside estimated investment need, with a RAG rating indicating whether current spend meets the estimated need (green), falls within 20% below it (amber), or is more than 20% below it (red). A confidence rating is assigned to each investment estimate, alongside the primary source from which the investment estimate was derived.

|

Sector |

Sub-sector / approach |

Investment estimate (£m) |

Investment estimate (£m/yr) |

2026/27 budget (£m/yr) |

Confidence |

Investment estimate source |

|---|---|---|---|---|---|---|

|

Agriculture |

£2,347m – £3,091m |

£167.6m– £220.8m | £167.6m – £220.8m | Low |

Scottish Government Budget | |

|

Communities |

Capacity building |

£102m |

£7.3m | £6.9m |

Medium |

Scottish Government Budget |

|

Property flood protection |

£885m – £1,102m |

£63.2m – £78.7m | £42m |

Low |

Scottish Government & DEFRA, HM Government | |

|

Property flood resilience |

£10.5m – £52m |

£0.8m – £3.7m |

Unknown |

Medium |

JBA Risk Management2025 | |

|

Natural environment |

Woodland creation |

£115m |

£8.2m | £2.3m |

Low – Medium |

Scottish Government Draft Climate Change Plan |

|

Peatland restoration |

£236m |

£16.8m | £5.6m |

Low – Medium |

Scottish Government Draft Climate Change Plan | |

|

Natural restoration |

£73m |

£5.2m | £5.2m |

Low – Medium |

NatureScot | |

|

Transport |

Rail[1] |

£1,582m – £4,734m |

£113m- £338.1m | ≈ £87.8m |

Medium |

Network Rail Scotland |

|

Trunk roads and motorways |

£1,418m – £2,213m |

£101.3m – £158.1m | £82.3m |

Very low |

Scottish Government Budget | |

|

Water |

Scottish Water[2] |

£1,067m – £2,466m |

£82.1m – £189.7m |

Unknown |

Medium |

Scottish Water |

|

Total |

£7,835.5m – £14,182.8m |

£565.5m – £1,026.6m |

The macroeconomic effects of investing in climate adaptation

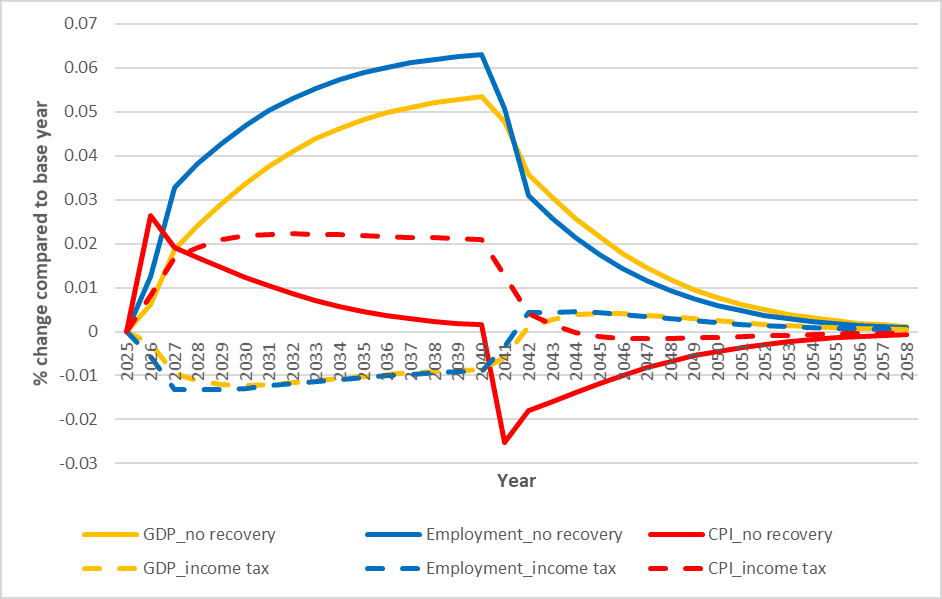

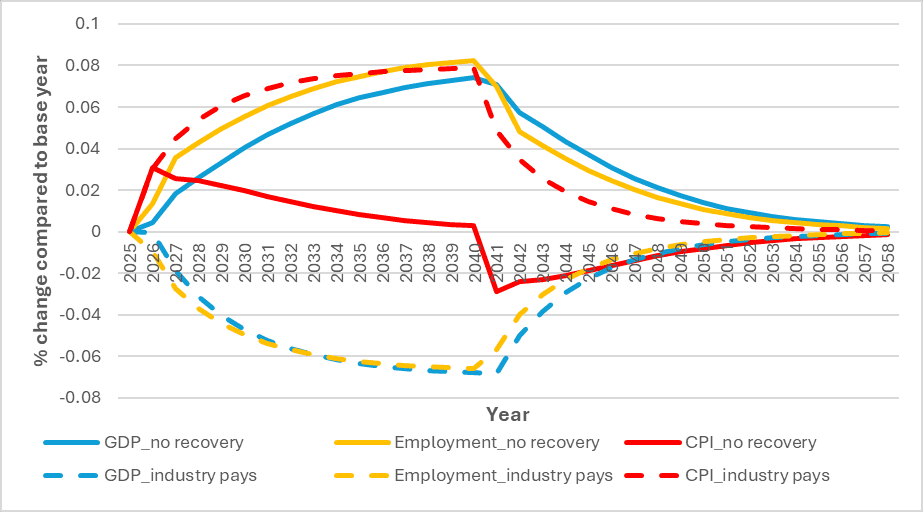

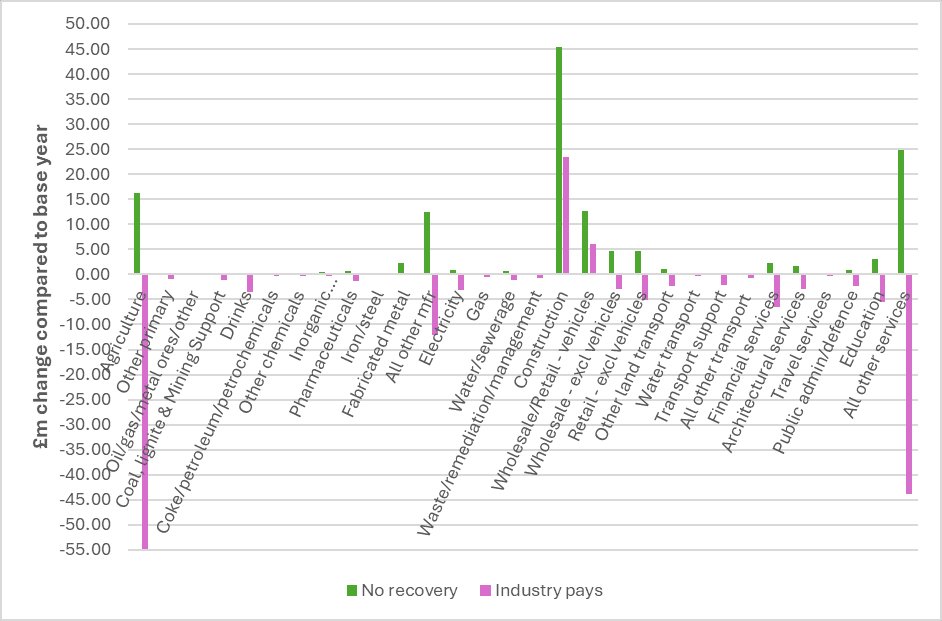

A full assessment of the macroeconomic costs and benefits of adaptation were beyond the scope of the study. However, the study did model the direct economic effects of adaptation spending across sectors. It also explored how different approaches to cost recovery affect economic activity, employment, and household incomes.

The modelling consistently shows that adaptation spending generates a positive economic stimulus during the investment period, supporting jobs and output particularly in construction, engineering, and land-based supply chains. However, the way costs are recovered matters considerably. Income-tax-based recovery is progressive but dampens household consumption and reduces activity in consumer-facing sectors. Charging-based approaches – such as higher food prices in agriculture or water bills in the water sector – tend to be regressive, falling disproportionately on lower-income households for whom essential goods represent a larger share of budgets. Recovery through public spending cuts generates the most widespread economic losses, particularly across service sectors. Funding design is therefore important to consider alongside investment scale.

These results should not be interpreted as a full cost-benefit assessment of adaptation. The modelling captures the demand-side effects of spending and cost recovery, but does not account for avoided climate damages, residual risks, or the broader triple dividend of adaptation.

How will costs be borne by households, businesses, and the public sector?

The study investigated how adaptation is currently funded in each of the sectors. Climate adaptation in Scotland is currently funded predominantly by the public sector. Central and local government fund and finance most adaptation-relevant expenditure across transport, flood management, water infrastructure, agriculture, and the natural environment. This is largely through existing budget lines that deliver multiple objectives alongside adaptation. However, households and businesses pay more than previously understood, through Council Tax and Non-domestic rates. Households and businesses also bear some costs directly, for example through property-level insurance and on-farm investments, but this remains modest in most sectors.

This balance is unlikely to shift fundamentally. Most of the adaptation investment – including flood protection, transport resilience, and natural flood management – generates little or no direct financial return and is therefore structurally dependent on public funding. Analysis suggests that approximately three-quarters of adaptation investment needs will require public financing regardless of innovations in private finance mechanisms.

Scope to boost private sector participation

The study reviewed the innovative funding and financing models being used internationally and within Scotland. Analysis found that there is modest potential to increase private sector participation in adaptation funding and financing across all five sectors, and a range of innovative mechanisms are emerging. These include parametric insurance in agriculture, biodiversity credits and voluntary carbon markets in the natural environment, green and resilience bonds for flood and transport infrastructure, and catchment co-investment models in water. However, several important caveats apply:

- Scaling private investment will not happen through market forces alone. It will require concerted public policy action, enabling conditions, and in many cases public co-financing to de-risk private investment. The private sector’s role is best understood as complementary to, rather than a substitute for, public adaptation finance.

- There is a critical distinction between private financing (where private capital provides upfront funding) and private funding (where costs are ultimately borne by the private sector rather than transferred back to government or consumers). Many instruments that appear to increase private participation in practice shift the funding burden, rather than share it. Policy ambitions to mobilise private capital should be assessed against this distinction.

- High benefit-cost ratios in the adaptation literature typically reflect societal and environmental returns, including non-market values that generate no cash flow. Private investors assess financial returns, incremental revenues and recoverable costs, which are considerably lower. Treating strong societal co-benefit ratios as evidence of private investment attractiveness risks generating unrealistic expectations about the scale of private finance that can realistically be mobilised.

Recommendations

The report lays out the following key recommendations, in no particular order:

Table 2: Key recommendations for further research and strategic priorities.

|

Theme |

Research priority |

Strategic priority |

|---|---|---|

|

Adaptation targets, objectives & risk tolerance |

|

|

|

Asset level vulnerability & investment pipelines |

|

|

|

Financial transparency & attribution |

|

|

|

Triple dividend evidence base |

|

|

|

Distributional impacts |

|

|

|

Cross‑sector collaboration |

|

|

|

Prioritisation |

| |

|

Private finance mobilisation |

| |

|

Monitoring and evaluation |

|

Glossary

|

Annual Average Loss (AAL) |

The expected average financial loss from flood events in any given year, calculated across all possible flood scenarios weighted by their probability of occurrence. |

|

Adaptation pathways |

A planning approach that sequences adaptation actions over time, allowing for adjustments as climate change and its impacts become better understood. |

|

Bottom-up costing |

An approach to estimating adaptation investment needs that builds cost estimates from detailed, project-level information gathered from engineers, contractors and technical specialists, or from specific policy objectives where budget lines can be scaled up. |

|

Computable General Equilibrium model (CGE model) |

An economic modelling framework that simulates the interactions between different sectors of an economy to assess the broader macroeconomic impacts of policy changes or external shocks, such as climate change. |

|

2026/27 Climate Taxonomy |

A classification system, published alongside the Scottish Government budget, that identifies budget lines according to their impact on climate change mitigation and adaptation. |

|

Community Benefit Funds (CBFs) |

A community benefit fund is a voluntary, typically annual, financial contribution provided by developers to local communities hosting major projects, such as renewable energy sites. |

|

Consumer Price Index (CPI) |

Presents the percentage change in prices that consumers pay for goods and services. |

|

Control Period (CP) |

Network Rail’s fixed five-year funding and planning cycle that sets budgets and outputs for the railway (e.g. CP7: 1 April 2024 – 31 March 2029). |

|

Expected Annual Damages (EAD) |

The average annual financial cost of flood damage calculated across return periods, accounting for both the likelihood and severity of events. |

|

Gross Value Added (GVA) |

A measure of the value of goods and services produced in an area, industry or sector of an economy, used here as a proxy for scaling adaptation investment estimates across countries. |

|

Major Capital Investment (MCI) |

Large-scale, transformational infrastructure schemes where continued operations would otherwise become impossible as a result of a changing climate. |

|

Natural Flood Management (NFM) |

An approach to reducing flood risk that works with natural processes, for example through wetland creation, tree planting or river restoration, to slow the flow of water and reduce peak flood levels. |

|

Organisation for Economic Co-operation and Development (OECD) |

An international, intergovernmental forum of 38 developed market-based economies established in 1961 to stimulate economic progress and world trade. Headquartered in Paris, it provides data, policy analysis, and standards to promote prosperity, equality, and well-being. |

|

Office for Budget Responsibility (OBR) |

The Office for Budget Responsibility was created in 2010 to provide independent and authoritative analysis of the UK’s public finances. |

|

Operations, Support, Maintenance and Renewals (OSMR) |

The category of Network Rail Scotland investment covering day-to-day operational response to weather, preventative and reactive maintenance, and asset renewals. |

|

Property Flood Resilience (PFR) |

Measures applied at the individual property level to reduce the risk of flooding or minimise flood damage, such as flood doors, air brick covers, or non-return valves. |

|

Potential Vulnerable Areas (PVAs) |

Areas identified by SEPA as being at significant risk from flooding, which form the basis for Flood Risk Management Planning in Scotland. |

|

Representative Concentration Pathway (RCP) |

A greenhouse gas concentration trajectory used in climate modelling to represent different possible futures based on varying levels of emissions (e.g. RCP 4.5 is a moderate emissions scenario; RCP 8.5 is a high emissions scenario). |

|

Residual damage |

The climate-related losses or damages that remain even after adaptation measures have been implemented, reflecting the limits of adaptation effectiveness. |

|

Scottish Environment Protection Agency (SEPA) |

Scotland’s environmental regulator, responsible for flood risk assessment, flood warning, and producing Scotland’s Flood Risk Management Plans. |

|

Scottish National Adaptation Plan 3 (SNAP3) |

The third Scottish National Adaptation Plan, covering 2024–2029, setting out actions to achieve five national outcomes for climate resilience across society, the economy and the environment. |

|

Scottish National Adaptation Plan 4 (SNAP4) |

The fourth Scottish National Adaptation Plan will cover 2029 – 2034, setting out actions to better adapt Scotland to the changing climate. |

|

Strategic Review 27 (SR27) |

Scottish Water’s regulatory investment planning period covering 2027–2032, within which adaptation investment needs are assessed and costed. |

|

Sustainable Urban Drainage Systems (SUDS) |

Drainage infrastructure designed to manage surface water in a way that mimics natural drainage, reducing flood risk, improving water quality and enhancing the urban environment. |

|

Top-down costing |

An approach to estimating adaptation investment needs that uses economic models and sector-level damage assessments to derive aggregate cost estimates, typically without detailed project-level information. |

|

Triple dividend |

The three categories of benefit that adaptation investment can deliver: (1) avoided climate losses; (2) wider induced economic benefits such as infrastructure investment stimulus; and (3) social and environmental co-benefits such as biodiversity gains and improved mental health. |

|

UK Climate Projections 2018 (UKCP18) |

The most recent set of probabilistic climate projections for the UK, produced by the Met Office, used to inform climate risk assessments and adaptation planning across multiple sectors. |

|

Value transfer |

A method of estimating costs or benefits by applying findings from existing studies in comparable contexts (e.g. other countries or regions) to a new setting, adjusted for relevant differences such as economic scale or population. |

Introduction

Overview, aim and scope

Tackling the climate emergency is a priority area for the Scottish Government – alongside eradicating child poverty and growing the economy and delivering high quality sustainable public services (Scottish Government, 2025a). As part of tackling the climate emergency, three questions have emerged associated with the need to better understand:

- The costs of the Scottish Government climate change ambitions for adaptation and the residual damage of necessary trade-offs.

- The macroeconomic effects of climate impacts and adaptation.

- How these costs are being met today, and options for how these costs will be met by different groups, including public and private sectors.

This project provides an initial exploration of some of these issues. In doing so, it supports the Scottish Government in developing an evidence base on the potential costs of climate adaptation across a range of sectors. This is important information to assist in strategically planning and driving forward future adaptation action, in line with Scotland’s National Adaptation Plan.

The analysis focuses on three interconnected research objectives:

- Estimate adaptation investment needs for five sectors – agriculture, communities (focusing on flooding), natural environment (woodland creation, peatland restoration and nature restoration), transport (trunk roads and motorways and railways), and water (supply and treatment) – until 2040. This should be aligned with the with adaptation objectives defined in the Scottish National Adaptation Plan 3 (SNAP3) 2024–2029;

- Assess the likely investment split, over time, between the public sector, private sector businesses and individuals for each sector; and

- For each sector, identify the potential to support private sector participation in funding and financing adaptation, highlighting barriers to scale, and recommending policy instruments to mobilise private capital.

Context: climate risks in Scotland

Scotland’s businesses, infrastructure, communities and environment are becoming increasingly exposed to climate change. These impacts carry serious economic consequences.

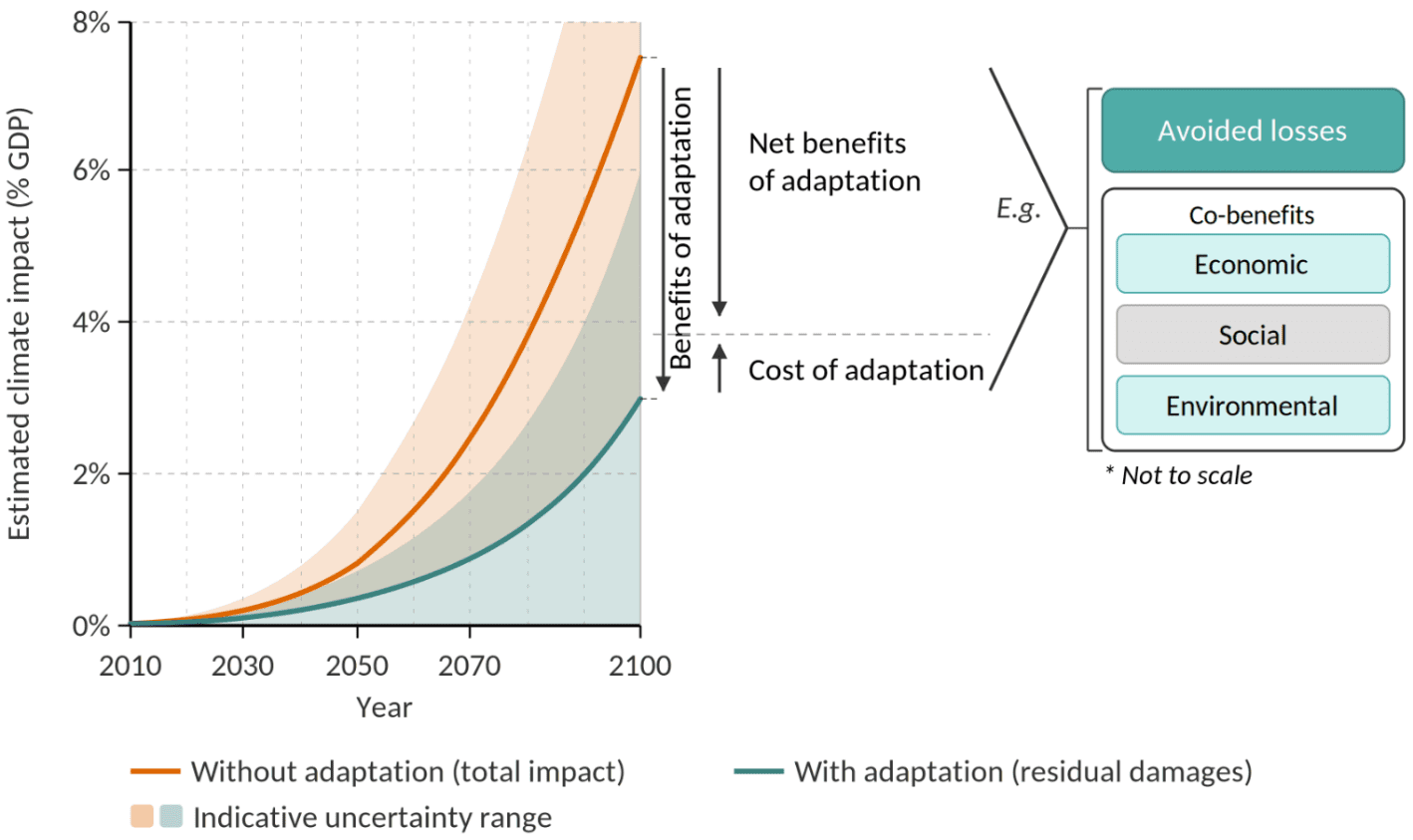

The estimated impact of climate change on the UK’s economy differs depending on the climate scenarios used and wider socio-economic assumptions made within modelling. This study assessed the results for Scotland using results from a major EU project (Bosello et al., 2020). Across several climate scenarios, these suggests that from 2030 Scotland’s economy could be 0.3 – 0.5% smaller each year. By 2050, losses could rise to 1.2 – 1.6%, increasing further to 1.5 –3.3% by the 2070s. These are shown in Figure 1, and have been used as the basis for supporting subnational assessments of economic impacts in Scotland (e.g. Climate Ready Clyde, Highland Adapts, South East Scotland and Forth Valley).

Figure 1: Projected impact of climate change on GVA in Scotland for a range of future climate scenarios using Shared Socioeconomic Pathways 2 (SSP2). High Investment Mobility. SSP2 is also known as ‘middle of the road’ and assumes the world follows a path in which social, economic and technological trends to not shift markedly from historical patterns…

A second study, Rising et al. (2022), included additional risks, such as low-probability high-impact events, projecting that under current policies – and compared to a 2000 baseline – the total cost of climate change damages to the UK are projected to increase from 1.1% of GDP at present to 3.3% by 2050 and up to 7.4% by 2100 (Rising et al., 2022). Furthermore, the Office for Budget Responsibility (OBR) estimate that the cost of climate change could even reduce the UK level of GDP by 8% by 2070 if the world was to warm by 3oC by the end of the century (Office for Budget Responsibility, 2025).

While adaptation can significantly limit climate related damages, fully eliminating climate risk is neither technically feasible nor economically rationale (Rexer & Sharmer, 2024). This means that even robust adaptation actions will leave some residual risk, highlighting the need to target measures that deliver the greatest benefit relative to their cost.

The Climate Change (Scotland) Act 2009 requires a National Adaptation Plan to be published every five years, aligned with the latest UK Climate Change Risk Assessment (CCRA). The latest, SNAP3, covers 2024 – 2029. SNAP3 sets out outcomes, delivery objectives and policy actions. It the first UK Adaptation Plan to also be supported by a monitoring and evaluation framework to track progress. However, specific objectives around risk reduction, as well as associated costs or budgetary allocations remain undefined in Scotland and across the UK.

As the Scottish Government prepares to receive the upcoming fourth UK Climate Change Risk Assessment (CCRA4) and Well Adapted UK report, there is growing recognition of the need to be more specific about the assumptions underpinning adaptation planning, and the costs and benefits. The Climate Change Committee (CCC) recommends that the Scottish Government introduce quantified, timebound adaptation targets to better track progress and strengthen accountability, consistent with preparing for +2°C warming by 2050 while managing risks associated with up to +4°C by the end of the century (Scottish Government, 2025b). However, setting such targets requires clarity on the level of climate risk that government and society are willing to tolerate.

This raises the important question of the acceptable level of risk, and for whom. Different communities, sectors and social groups will be affected in different ways. Given these complexities, developing adaptation targets will likely require broader engagement, including opportunities for the public and stakeholders to contribute to discussions about acceptable levels of risk. It also involves considering who pays – raising questions of equity and risk ownership. As such, adaptation target setting can be closely linked to Just Transition principles.

Defining the level of climate risk that is acceptable is therefore closely associated with the question of how much adaptation investment is needed, and who should pay for it.

Yet current evidence on these questions for Scotland is limited. There are partial estimates of adaptation investment need within the literature, but no agreed sector-specific adaptation targets, no systematic estimates of the investment required to meet them, and no established framework for understanding how costs should be shared between the public sector, private sector, and individuals.

This gap matters: without a clearer picture of adaptation investment needs, it is difficult to plan strategically, allocate budgets effectively, or make the case to mobilise private capital alongside public expenditure. But it is also challenging due to the deep uncertainty of climate change – including our warming trajectories and socioeconomic change.

This report seeks to begin closing that gap. Drawing on a range of analytical methods and the best available evidence across five sectors – agriculture, communities (flooding), transport, water, and the natural environment – it provides indicative estimates of Scotland’s adaptation investment needs to 2040, an assessment of public-private investment splits, and an exploration of opportunities to increase private sector participation in financing Scotland’s adaptation.

This report is structured as follows:

- Section 2 sets out a general account of the economics of adaptation. This sets out the conceptual framework for estimating investment needs, and approaches exploring the public-private investment split. It also positions the existing evidence base for Scotland.

- Section 3 presents our approach and methods.

- Section 4 provides sector-specific results for agriculture, communities (floods), the natural environment, transport, and water. It explores adaptation investment needs, macroeconomic effects and wider impacts, and funding and financing arrangements across all five sectors.

- Section 5 presents a summary of our analysis

- Section 6 outlines recommended research and strategic priorities.

The economics, costing and financing of adaptation

The economics of adaptation

In simple terms, adaptation costs and benefits can be estimated by first assessing the current and future impacts of climate change, then evaluating how much these impacts can be reduced and at what cost (Boyd and Hunt, 2004; UNFCCC, 2009). Adaptation measures can substantially reduce damages, but even well-designed strategies involve trade-offs: investing more in adaptation may deliver greater risk reduction but also increases cost. As a result, reducing risk to zero is neither technically feasible nor economically desirable, and some residual risk will always remain (Rexer & Sharma, 2024).

The scale of costs and benefits depends heavily on chosen objectives. For example, whether aiming for economic efficiency, reducing risks to acceptable levels, or maintaining today’s relative level of climate risk despite worsening conditions. In practice, estimating adaptation costs is highly complex because of deep uncertainty, with issues of socioeconomic change, future emissions, climate models, regional scenarios, impacts, adaptation responses, and political priorities combining to make modelling challenging (Wilby and Dessai, 2010; Taylor et al., 2025; Valverde et al., 2022). These uncertainties make it challenging to assess costs and benefits, creating the potential for over or underestimation of investment.

Despite this, there are some examples. These include national design standards for flood risk (e.g.to a 1-in-200-year event in Scotland, or up to 1-in-10,000-year in the Netherlands (Westerhof et al., 2023)), and emerging work on resilience in warming trajectories more broadly. The UK Government’s Long Term Investment Scenarios explore the optimum levels of investment under different climate scenarios and then use that to guide the spending envelope in the UK’s Flood and Coastal Erosion Risk Management (Environment Agency, 2021). And on reference scenarios, the Climate Change Committee has advised the UK Government to plan for 2 degrees of warming and prepare for 4, while in France the French Government has adopted a reference trajectory of four degrees.

Furthermore, adaptation investment can deliver multiple co-benefits, collectively known as the ‘triple dividend’ (Global Commission on Adaptation, 2019):

- The first dividend relates to avoided losses from successful adaptation. For example, a home that doesn’t flood because flood defences were built.

- The second relates to induced economic benefits such as the stimulus to the economy. For example, from capital investment in infrastructure development projects.

- The third includes social and environmental benefits. For example, afforestation projects that slow water runoff to rivers provide flood mitigation but also deliver biodiversity gains, carbon sequestration, and mental health benefits through green space access.

Considering all three dividends has the potential to improve the economic rationale of investing in climate change adaptation (Figure 2). In this report, while our analyses partially explore triple dividend benefits, it is beyond the scope of work to comprehensively consider wider savings made on triple dividends (see Section 8 on next steps).

Figure 2: The economics of adaptation. The orange line shows projected climate change impacts on GDP (%) without adaptation; the teal line shows residual damages with adaptation. The gap between them represents the gross benefits of adaptation – subtracting the cost of adaptation yields the net benefits, comprising components such as avoided losses and economic, social and environmental co-benefits. Shaded areas indicate indicative uncertainty ranges only. The benefit breakdown is illustrative and not to scale. Adapted from Boyd and Hunt (2004), Global Commission on Adaptation (2019), and Watkiss et al. (2026a).

Apportioning adaptation costs

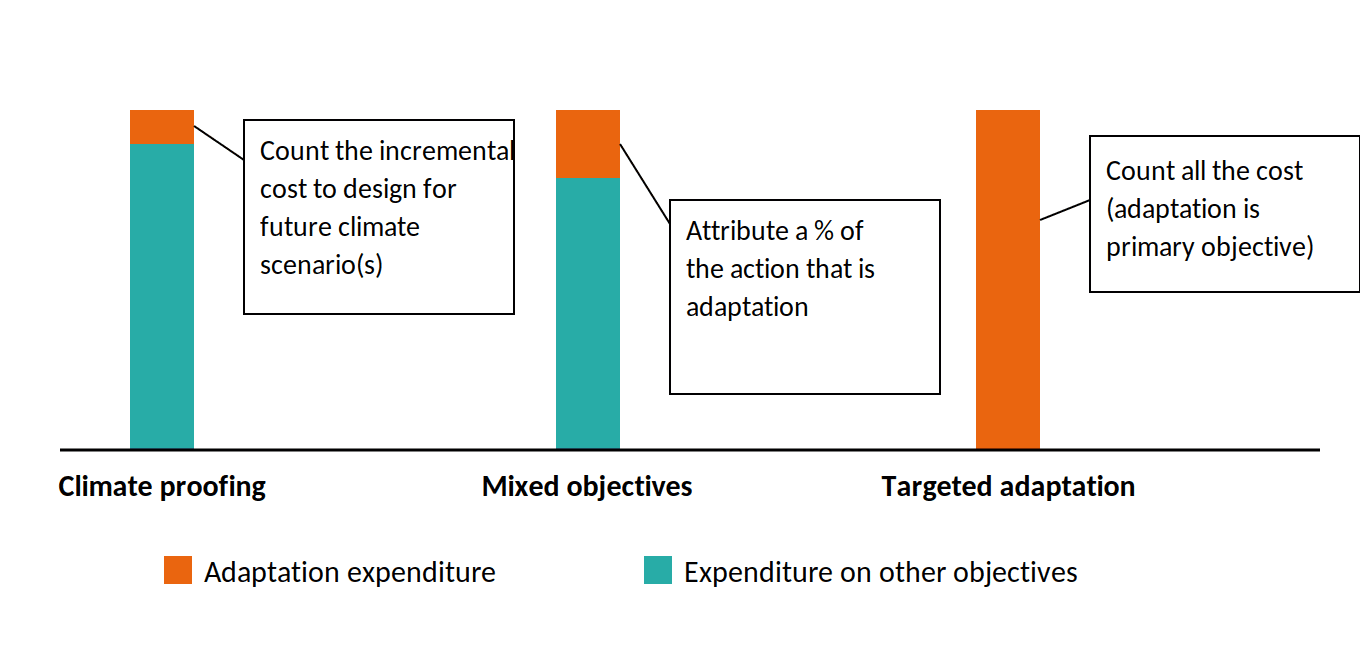

A key challenge in estimating adaptation investment needs is defining what constitutes ‘adaptation’ and how to attribute costs when activities serve multiple purposes. Climate adaptation rarely occurs in isolation – it is typically integrated into broader investment programmes, delivered alongside other policy objectives, or embedded within routine infrastructure maintenance and renewal. This raises practical questions for cost estimation: should we count the full cost of a project that includes adaptation as one of several objectives, or only the incremental cost of climate-proofing measures above a baseline investment?

To address this, the study adopted the adaptation cost taxonomy developed by the Multilateral Development Banks (MDBs), which has been widely applied internationally to track adaptation finance and compare investment needs across countries (MDB, 2022). This taxonomy categorises adaptation investments into three types based on the role adaptation plays in the overall investment (Figure 3):

Figure 3 Taxonomy of adaptation costs. Adapted from Watkiss et al. (2026a) based on Multilateral Development Banks (2023).

- Building climate adaptation into proposed programmes and investments (climate proofing). For example, to include climate change in the design standards for new road investments. In this case, adaptation is not a major objective. Instead, assessments investigate the incremental costs of adaptation, over and above the core programme / investment costs.

- Targeted/pure adaptation programmes and investments (targeted adaptation). In this case, the primary objective of the policy, programme or project is adaptation to climate change. For example, investing in coastal flood protection to address sea-level rise. In this case, the total costs of the investment are counted as adaptation.

- Investments with multiple benefits that include adaptation (mixed objectives). Sitting between the two extremes above are a set of cases where adaptation is one of several objectives of the policy, programme or project (a secondary or significant objective). For example, investing in peatland restoration will lead to greater resilience of the peatland (to climate change) as well as off-site benefits (water management) but this investment is primarily associated with biodiversity and ecosystem services. In this case a proportion of the cost is attributed to adaptation, but this is often difficult to do accurately and involves more subjective decisions.

These distinctions are important for climate adaptation investment estimation and the economic rationale for investment. However, this categorisation can create potential for confusion in practice. Activities that might have been pursued primarily for economic development, environmental restoration, or other policy goals can be classified as ‘adaptation’ if they deliver climate resilience benefits – even when adaptation was not the original or primary driver. This raises important questions about additionality: would the investment have proceeded anyway without climate considerations?

Approaches to costing adaptation investment

International approaches

There is no single ‘correct’ method for costing climate adaptation. Instead, there are a variety of approaches, and the most appropriate approach depends on the context. Factors such as specific objectives, analysis level, measure types, and critically, the available data and resources all influence the choice (World Bank, 2024; Taylor et al., 2025).

Climate adaptation objectives can be framed in several ways – by setting targets based on future warming levels, engineering resilience standards, specific risk reduction goals, economic thresholds, or process-based requirements (World Bank, 2024). Each framing influences the scale of action, investment needs, and acceptable levels of residual risk. These choices shape how ambitious adaptation efforts must be, the types of projects prioritised, and the balance between public, private, and household responsibilities. Higher resilience standards typically require greater upfront investment, while economic optimal or process-based approaches may lower costs but leave more risk unaddressed (Taylor et al., 2025).

Costing methodologies exist on a spectrum: ‘top-down, science-first’ approaches use economic models and sector-level damage assessments to estimate aggregate costs, while ‘bottom-up, policy-first’ approaches build estimates from detailed project-level information gathered from contractors, engineers, and technical specialists, focused on answering specific near-term questions. There are also hybrid methods that blend top-down and bottom-up approaches. The World Bank identifies various tools and approaches for both sets of methods including top-down sector integrated assessment models (IAMs), computable general equilibrium (CGE) models, through to bottom-up sector-based costing, climate adaptation markups, and budget tagging approaches at the more granular level (World Bank, 2024).

The most accurate estimates for appraisal or project delivery come from bottom-up costing based on detailed contractor quotes. However, this approach requires substantial resources, data availability, time, and technical capacity to progress projects through to a level of maturity which can provide this, and this is not always available (Taylor et al., 2025).

European estimates

Multiple European countries have recently attempted to quantify their national adaptation investment needs, each developing similar, yet distinct, methodologies suited to their institutional context and data landscape. To inform the approach to Scotland, this study reviewed literature from these studies and drew key lessons from each, as follows:

Austria took a parallel approach (Knittel et al. 2017), adopting a top-down budget review using expert interviews to assign flexible apportionments of current spending to climate adaptation (such as 60% for flood infrastructure for example) and bottom-up costing of 67 National Adaptation Strategy measures grouped into cost bands. The two methods produced different results, €488m/yr versus €385m/yr respectively, revealing they measured fundamentally different things: current government activity versus strategic intent (Knittel et al., 2017).

France compiled existing estimates across 15 policy areas, gathering what stakeholders had already produced and providing unit-cost benchmarks from completed projects. It was openly acknowledged this represented ‘what exists’ in planning discussions rather than rigorous comprehensive costing (Dolques et al., 2025).

Spain aggregated funding from multiple sources, historical environmental spending, COVID recovery allocations, and department budgets, applying different percentages based on how directly measures addressed adaptation (100% for flood defences, 40% for ecosystem restoration, 10% for co-benefits). This reached €1.55bn for 2021-2025, though many costs remained undefined and excluded (MITECO, 2020).

Bulgaria grouped measures into Low/Medium/High-cost bands (up to €1m, €1-100m, over €100m) but using specific figures where detailed studies existed, such as €347.81m for irrigation from cost-benefit analysis (Dale & Zhekova, 2019).

Croatia took a strategic approach, developing a prioritised 20-year portfolio of adaptation investments (€3.6bn) through climate modelling and stakeholder workshops, then justifying the annual cost (€183m) by showing it was less than current average damages from extreme weather (€295m) (Croatian Parliament, 2020).

EU level analysis by Neumann et al. (2025) compiled national studies, adjusted them for different emission scenarios and hazards, then extrapolated to countries lacking data using sector economic output as a proxy. Transport estimates drew on seven national studies while agriculture relied on only three, highlighting persistent data gaps (Neumann et al., 2025). A separate EU level study (European Commission, 2026) conducted a bottom-up analysis, which reviewed member state risk assessments, identified and costed relevant measures and then scaled them to the EU. This suggests annual investment needs of €69bn/year to 2050, dominated by infrastructure and ecosystem investments.

There have also been estimates for the UK. These have focused on the costs of adaptation today by categorising actions in the National Adaptation Plan (NAP) in line with Multilateral Development Bank (MDB) taxonomies and estimating investment needs (Watkiss et al., 2026a), though there have been some estimates for future costs as part of the forthcoming Well Adapted UK report (e.g. in Watkiss et al, 2026b and others).

All these studies were transparent about the limitations of the methods used, acknowledging uncertainty rather than presenting false precision. They demonstrated that pragmatic, evidence-led approaches are essential given current data constraints, and framed estimates as ‘evolving documents’ requiring iterative refinement, not as definitive adaptation investment estimates.

Existing estimates for adaptation investment need

Globally, climate finance flows have grown significantly, with total flows reaching US$1.9 trillion in 2023 and private contributions exceeding US$1 trillion for the first time. However, the vast majority of this is directed towards mitigation, with Climate Policy Initiative (2025) estimating only 3.4% is going towards adaptation. The latest United Nations Environment Programme (UNEP) estimates show that developing countries will need at least US$320bn/yr – $400bn/yr for adaptation by 2035, which is roughly ten times higher than today’s international public adaptation finance flows (Watkiss and England, 2025).

To date, there has been limited research specific to Scotland on climate change adaptation investment need. Estimates are instead deduced from broader studies, ranging from £196–£1,340m per year:

- A recent World Bank study suggests that near-term adaptation investment for the EU27 could amount to 0.1% – 0.4% of GDP annually by 2030 (World Bank, 2024). Scotland’s Climate Emergency Response Group (CERG) applied these values to Scotland, estimating £196 – £784m per year by 2030 (CERG, 2024).

- Indicative estimates for the UK suggest adaptation costs of around £5bn/yr to 2030 for a subset of priority risks, rising to £10bn/yr or more when all 61 CCRA3 risks and proactive adaptation measures are included (Watkiss, 2022). These figures are expected to increase significantly after 2030 as the number of high magnitude climate risks grows from 12 to 21 by the 2050s. Yet these estimates remain partial and indicative, with substantial gaps in sectoral coverage, inconsistent assumptions, and a bias toward engineering solutions rather than social or institutional adaptation (Watkiss, 2022). Using Watkiss (2022) values, and assuming Scotland accounts for 7.5% share of UK economic output as a proxy (Harari & Murray, 2024), implies adaptation costs of approximately £375 – £750m per year.

- Analysis by the Office for Budget Responsibility (OBR) suggests adaptation costs of around 0.3% of GDP per degree of warming (OBR, 2021). The OBR also highlights that adaptation costs are likely to rise unevenly over time, with larger and more frequent economic shocks expected later in the century. Using 2024 prices, these costs are equivalent to £670 – £1,340m per year for Scotland under 1 – 2°C of warming respectively.

Scotland’s specific vulnerabilities and policy landscape mean these broader UK estimates may not accurately reflect Scotland’s climate adaptation investment need. For example, Scotland faces a distinctive combination of climate hazards and geographic contexts. This includes a higher proportion of woodland and peatland, topographic challenges, and 93 inhabited islands, that may not be captured by downscaling UK-wide estimates based on Scotland’s share of GDP. The CCRA3 Scotland summary is also the only national summary to identify flooding as the most severe and costliest hazard to businesses, further highlighting the limitations of direct comparison to UK-level estimates.

Investment need will also vary within Scotland, with some regions more vulnerable to climate risks. Nascent estimates of the public sector adaptation gap in Glasgow City Region (Climate Ready Clyde, 2021) suggested a gap of £187m in 2018/19 alone for the region’s local authorities and the health board, equivalent to around 2% of combined local authority and NHS expenditure across the region’s eight councils and two health boards. No other regional estimates in Scotland have been published.

While national climate adaptation investment estimates are lacking, some public bodies, such as Scottish Water and Network Rail Scotland, have conducted bespoke asset climate vulnerability assessments and initial adaptation cost estimates to facilitate strategic business planning (e.g., Network Rail Scotland, 2024; Scottish Water, 2025). Others have more limited research on specific adaptation investment need. Therefore, while some sector specific information exists, it is fragmented.

As well as absence of Scotland-wide adaptation estimates, there is a lack of robust estimates of the wider returns from adaptation investment. These include avoided climate damages, economic benefits, and broader socio-environmental gains that comprise the ‘triple dividend’ of adaptation.

Who pays for adaptation?

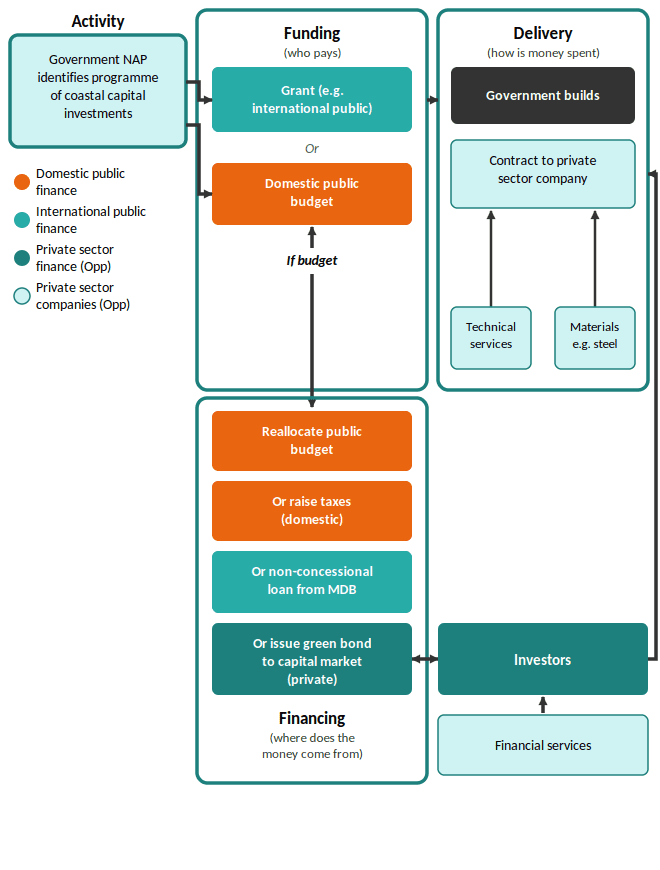

Financing versus funding

A critical but often overlooked distinction in climate adaptation investment is the difference between financing and funding (Watkiss and England, 2025). Financing refers to where the upfront money comes from, whether public grants, government borrowing, sovereign green bonds, or private capital, and the financial instruments and terms involved. Funding, by contrast, refers to who ultimately pays for the adaptation over the lifetime of the investment, whether through public budgets, taxation, or user charges. This distinction matters because private sector involvement can help close the financing gap without necessarily closing the funding gap: costs may simply be transferred back to governments or households rather than genuinely shared.

This is illustrated in Figure 4, which shows options for delivery of a programme of coastal flood protection in a developing country context. Here, the delivery is provided by the private sector, who build the contract. The financing can be provided in many ways, including from public budget, tax rises, or private sector financing through the capital markets. These are important since there is much greater potential for private sector financing than for developing business. For example, it is possible to attract significant amounts of private sector financing to support public sector investment, but ultimately government repays with interest. Therefore, it is important to consider whether we are seeking to boost private sector funding (i.e. the proportion of companies and businesses that actually contribute to the costs of adaptation), or merely the financing.

Figure 4: A simple example of the financing, funding, and delivery of adaptation for coastal protection. Source: Watkiss and England. 2025.

The role of public and private sectors

In recent years, there have been substantial efforts to better understand the factors which can inform whether such activities should be funded by the private or public sectors. These include whether the costs and benefits of activities are public or private as well as the level of financial returns they offer. These can be none/limited (and are therefore typically public), below-market or market level returns (OECD, 2023). The level of market returns for many adaptation options have been classified in Table 3, and these have been reviewed and updated to be relevant to the sectors in scope of this study:

Table 3 – Adaptation activities and potential returns in developed countries for the sectors explored in the study. Updated from Watkiss and England, 2025 and OECD, 2023.

|

Sector and activity |

Typical nature of investment |

Typical level of return | ||

|

Public |

Below market |

Market | ||

|

Coastal, river and surface water flood | ||||

|

Protection (coastal and river floods) |

Public |

ü | ||

|

Early warning services |

Public |

ü | ||

|

Natural flood risk management / NbS |

Public |

ü | ||

|

Property Level Flood Resilience and Resistance |

Private |

ü |

ü |

ü |

|

Water | ||||

|

Integrated water resources management (IWRM) |

Public |

ü | ||

|

Supply and distribution |

Mixed |

ü |

ü |

ü |

|

Demand management, inc. efficiency measures |

Mixed |

ü |

ü |

ü |

|

Agriculture | ||||

|

Research and Development |

Mixed |

ü |

ü |

ü |

|

Extension services |

Mixed |

ü |

ü |

ü |

|

Climate-smart agriculture |

Mixed |

ü |

ü |

ü |

|

Irrigation |

Mixed |

ü |

ü |

ü |

|

Trade and trade infrastructure |

Mixed |

ü |

ü |

ü |

|

Infrastructure | ||||

|

Transport (road and rail) |

Mixed |

ü |

ü | |

|

Biodiversity and Ecosystems | ||||

|

Protected areas |

Public |

ü |

ü | |

|

Capacity building, institutional strengthening, awareness |

Public |

ü |

ü | |

|

Forestry |

Mixed |

ü |

ü |

ü |

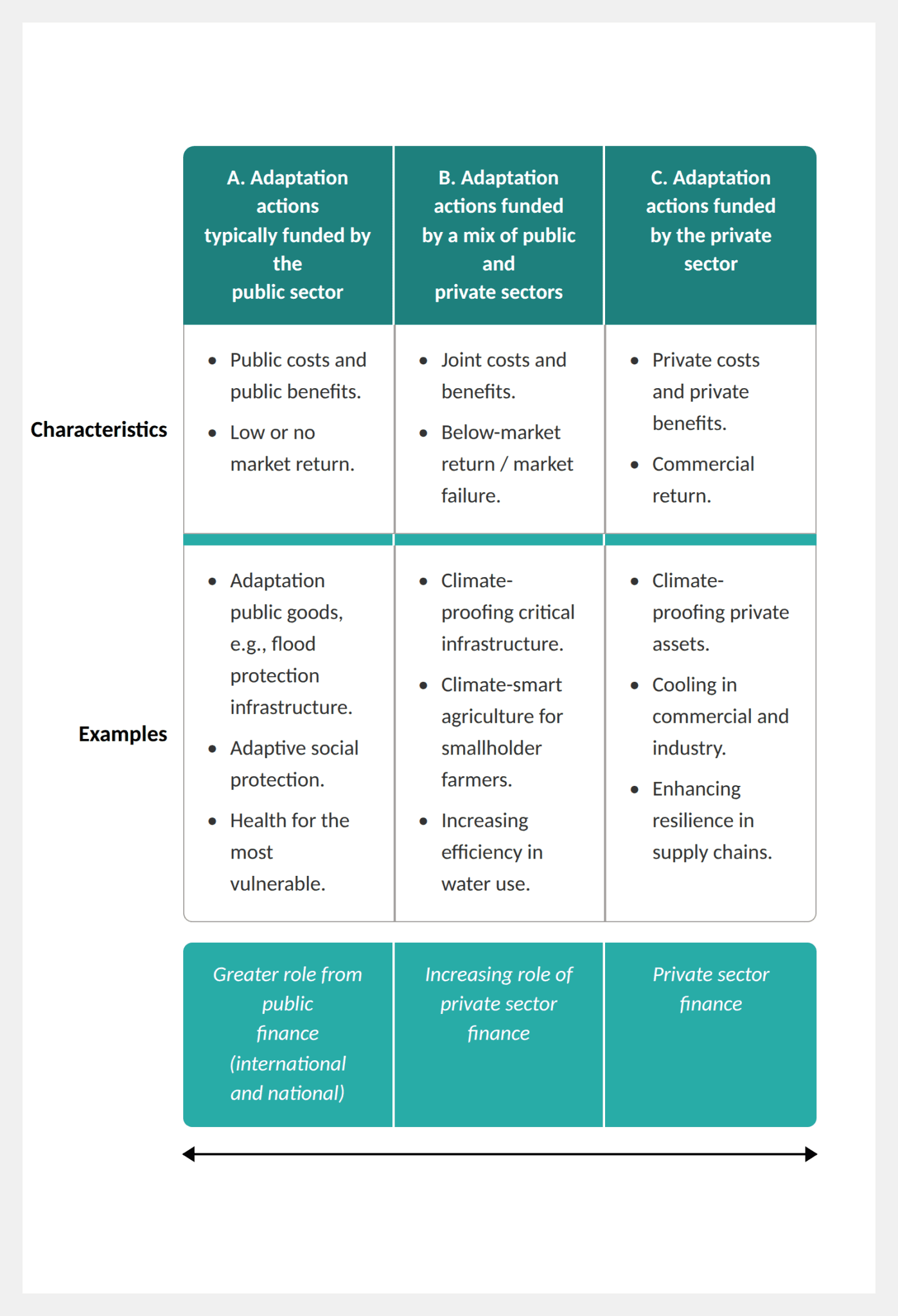

Building on this approach, UNEP (2025) outline a useful typology (adapted into Figure 5) for understanding where public and private actors are best placed to act, based on the combination of level of returns and whether the costs and benefits are public, private or joint. These can be used to help classify a broad range of activities which are funded by either the public sector, private sector, or a mix of both.

Type A actions are public goods, such as major flood protection schemes, that generate little or no financial return and are therefore typically initiated and funded by government. Type B actions involve a mix of public and private costs and benefits, and where returns are typically below market. For example, supporting climate-smart agriculture. These typically involve blended finance arrangements. Type C actions sit within existing well-functioning markets and generate commercial returns, such as industrial cooling systems, and would be expected to be entirely privately financed and funded.

Figure 5: Simplified categorisation of adaptation types (A-C) and opportunities for private sector engagement. Adapted from UNEP (2025).

Barriers to adaptation finance

Private sector investment in climate adaptation remains persistently low, despite adaptation often delivering high economic returns for society (World Bank, 2024).

The core problem is that while the societal benefits of adaptation can be substantial, the financial returns that matter to private investors are much lower. Adaptation frequently reduces losses or damages and generates limited revenues, making it difficult to construct a viable business case for private finance. This is especially the case, given the opportunity cost of capital, and difficulties of modelling climate-related disruption in cashflows and returns (Watkiss and England, 2025). There are also issues of discounting, where costs arise today, but benefits occur far in the future and are therefore higher. The private sector also uses higher discount rates than the 3% in the public sector (HM Treasury, 2026), compounding this issue.

Many studies reporting high benefit-to-cost ratios for adaptation are measuring economic or societal returns, which include non-market benefits such as environmental value. Private investors, however, assess financial returns, incremental revenues and cash flows, which are considerably lower. This distinction is frequently misunderstood and leads to unrealistic expectations about the role private finance can play (Watkiss and England, 2025).

Watkiss and England (2025) identify five main categories of barrier to adaptation finance:

- Information barriers, including insufficient data on climate risks and limited investor understanding of adaptation as an asset class.

- Market failures, including public good characteristics and underdeveloped adaptation markets.

- Behavioural barriers, including low perceived urgency and limited willingness to pay for risk reduction.

- Policy and governance barriers, including weak or conflicting regulation and poor cross-sector coordination.

- Financial and bankability barriers, including long payback periods, small project sizes, high complexity, and limited replicability.

Scaling private investment into publicly identified adaptation priorities remains a significant challenge, particularly for smaller, fragmented projects involving many actors and beneficiaries.

Boosting private sector opportunities

Globally, current private sector contributions to climate adaptation are very small (approximately 3% of total needs). Even with substantial innovation and concerted effort, the private sector is expected to deliver only around 15% of required adaptation by 2035, with even less in least developed countries and small island developing states (Watkiss & England, 2025). However, this varies significantly based on country and sector structure. Recent analysis of the UK’s third National Adaptation Plan finds much higher numbers, suggesting around 45% of total adaptation costs are borne by private households and businesses (Watkiss et al., 2026a), in part driven by the privatised nature of the water sector in England. As Scottish Water is publicly owned, the equivalent figure for Scotland is likely to be lower, with a greater share of adaptation costs falling to the public sector.

As a result, climate adaptation is currently funded predominantly by the public sector, both globally and within the Scotland. Central and local government fund most adaptation-relevant expenditure across transport, flood management, water infrastructure, agriculture and the natural environment, largely through existing budget lines that deliver multiple objectives alongside adaptation, climate-proofing, or pure adaptation investment (e.g. for flood protection). Across all sectors, households and businesses also bear some adaptation costs directly. For example, through property level insurance or on-farm investments. However, this remains modest.

Crucially, scaling up private sector participation will not happen through market forces alone. It will require concerted public policy action, enabling conditions, and in many cases public co-financing to de-risk private investment. The private sector’s role is therefore best understood as being complementary to, rather than a substitute for, public adaptation finance (Watkiss and England, 2025).

Governments can adjust the financial characteristics of adaptation activities to increase private sector participation, either at the market level or at the level of individual investments. At the market level, this can include improving existing markets (e.g. through better provision of climate risk information), creating new markets (e.g. through water credits), or supporting public provision where markets fail (Greenhill et al., 2026). At the level of individual investments, policy and regulation or blended finance arrangements can be used to alter financial characteristics and improve commercial viability (World Bank, 2019; Watkiss and Ward, 2025). Where neither approach is sufficient, there remains scope to diversify the range of public financing sources and instruments. This is illustrated in the decision tree in Appendix A.

Climate justice considerations

Another significant consideration within the costs of adaptation are the distributional aspects, and the need for a “just resilience”. The CCC report to Scottish Government on climate adaptation and just transition in 2022 highlighted that fairness in adaptation is strongly linked to just transition concepts, and it is crucial to consider distributional effects to ensure effective and fair adaptation (CCC, 2022). Several characteristics that lead to increased vulnerability and reduced adaptive capacity to climate risk were identified, and include low-income groups, the very young and the elderly, and those in rural regions. The CCC recommended that policy to help address adverse distributional impacts should be routed in an understanding of the distributional effects of climate risks and opportunities.

While climate risks are unevenly distributed and demand equitable responses (European Environment Agency, 2025), they also involve costs. Such costs can be explored from several perspectives. A simplified set of approaches is shown in Table 4, ranging from most targeted to those most socialised, though in reality the approach may be context specific.

Table 4: Indicative approaches to guide who should pay for adaptation: Adapted from Paul Watkiss Associates.

|

Approach |

Description and examples |

Justification |

|

Costs borne by those at risk |

Those directly exposed to risks bear the costs of adaptation (e.g. PFR) |

Beneficiaries should pay costs |

|

Costs socialised amongst users |

Investment in water / rail networks for adaptation through water bills and ticket sales |

Efficiency, user pays |

|

Maximise social welfare – prioritise dense population |

Use of Cost-Benefit analysis to maximise (e.g. flood defences in England) |

Social welfare, cost effectiveness |

|

Costs socialised across society |

Adaptation of nature and biodiversity, flood protection |

Public goods, fairness or equity |

|

Adaptation responsibility based on historic and current emissions |

Highest emitters pay for adaptation (e.g. Green Climate Fund, Adaptation Fund) |

Adaptation costs driven by historic emissions / most wealthy |

The CCC recommended that policy to help address adverse distributional impacts should be rooted in an understanding of the distributional effects of climate risks and opportunities.

Early work underway globally is considering some of the principles behind the costs of adaptation. The Government of New Zealand (2025), set out some early principles in its National Adaptation Framework such as ensuring pre-and post-climate event costs are shared across society and over time, and that the public sector is used to incentivise private sector action, and to take market-based approaches that adjust over time. While beyond the scope of this report, it is noted that such considerations may have the potential to significantly vary relative distribution of costs.

Knowledge gaps and challenges

Evidence gaps in Scotland’s adaptation investment landscape

It is important to note here that adaptation investment, globally, is poorly understood, and many countries are, like Scotland, working to quantify their national adaptation investment needs. Scotland faces multiple knowledge gaps around climate adaptation investment. These include:

- No clear understanding of the total investment required across sectors, including whether this will involve millions or billions of pounds, or how this spending will be distributed with time.

- No detailed picture of what climate adaptation investment could deliver for different sectors.

- No specific, measurable, achievable, relevant and time-bound (SMART) adaptation objectives under SNAP3.

- No assessment of associated costs of not adapting, and/or expected residual damages.

- No budget allocation for each SNAP3 objective.

These knowledge gaps make it difficult to determine whether a financing gap exists or how large that gap might be in Scotland.

Broader knowledge gaps in Scotland and beyond include:

- Lack of robust estimates of the wider returns from adaptation investment, including avoided climate damages, economic benefits, and broader social and environmental gains that comprise the ‘triple dividend’ of adaptation.

- Limited research exploring opportunities for blended public-private funding partnerships to support climate change adaptation spending.

Further research on these broader topics is key to ensuring and prioritising just and equitable climate adaptation solutions in Scotland.

Box 1: Challenges and limitations

Estimating Scotland’s climate adaptation investment need is inherently challenging. This work provides an initial method, approach, and set of assumptions to estimate climate adaptation spending across sectors. It is intended as a first step that will require further development. The figures presented should therefore be treated as indicative, order of magnitude estimates rather than precise calculations. Readers and peers are encouraged to build on this analysis by adding new assumptions, incorporating additional sub-sectors or hazards, or testing alternative scenarios and risk-tolerance thresholds.

The key data limitations and challenges underlying these estimates include:

Baseline spending: Incomplete information on current adaptation expenditure across Scotland makes it difficult to establish a reliable baseline from which to measure progress or scale up investment.

Asset vulnerability: Comprehensive inventories of climate-vulnerable assets are lacking in most sectors, and there is limited understanding of how vulnerability will evolve as the climate changes.

Climate and socio-economic uncertainty: Projections of how Scotland’s climate will change over the coming decades remain uncertain, as does the evolution of the broader socio-economic and political landscape.

Risk tolerance: Without clearly defined government risk tolerance thresholds or adaptation objectives for each sector, it is difficult to establish an ‘end goal’ against which investment needs can be scaled.

Scope limitations: The analysis focuses on selected sub-sectors and key hazards; many relevant adaptation actions and climate risks across Scotland’s wider economy are not included.

Methodological assumptions: Estimates rely on assumptions regarding appropriate adaptation objectives for 2040 and whether spending continues at current levels or scales up in line with growing climate risks.

Study methods

Our approach

Scotland faces similar challenges in estimating climate adaptation investment need to those across Europe, and the fragmented data landscape means no single method could be applied consistently across all sectors. The study therefore adopted a pragmatic, multi-stage and multi-method approach:

- estimating adaptation costs for each sector using the most appropriate costing method given available evidence;

- feeding these into a macroeconomic model to explore the economic impacts of different financing routes;

- mapping current governance arrangements to understand how adaptation is being paid for today; and,

- exploring the potential to increase private sector participation.

Due to resource and data limitations, the three analyses were conducted separately, with differing underlying assumptions. The cost estimates, macroeconomic modelling, and funding analysis are therefore not directly comparable with one another. Each is intended as a broad exploratory assessment, and further integrated analysis would be needed to draw firm conclusions across all three components.

Throughout, developing robust estimates also required identifying which SNAP3 targets and objectives are relevant to each sector and considering wider socio-economic context beyond climate risk alone. The detailed steps are shown below.

Step 1: Adaptation costing

Adaptation objective setting

We adopted 14 of the 23 objectives set out in SNAP3 (Scottish Government, 2024a). The selected objectives covered four of the five broader SNAP3 outcome areas identified by the Scottish Government: Public Services (PS), Economy, Business & Industry (B), Nature Connects (NC), and Communities (C) (Scottish Government, 2024a). Objectives relevant to the fifth SNAP3 outcome area, Connected and Engaged Society (CE), were not included in the scope of this analysis. The specific sectors, objectives and corresponding outcome explored within our analysis area are summarised in Table 5.

Table 5: Climate change adaptation outcome area and objectives from SNAP3 that align with the five sectors considered in our work were selected and, where relevant, amended. Sectors not explored – due to resource constraints – are crossed through in the objectives below.

|

Sector |

SNAP3 outcome area and objectives |

|---|---|

|

Agriculture |

B2: Farming, |

|

Communities |

C1: Regional collaborations are driving inclusive, effective and place-based adaptation across all of Scotland. |

|

C2: Communities and individuals are supported, informed, and able to take locally led adaptation action, supporting local priorities and resilient, healthy, and equitable places. | |

|

C3: Communities and individuals are able to prepare for, respond to and recover from emergencies in a way that builds future climate resilience, complements the work of emergency responders and protects those with vulnerabilities to multiple risks. | |

|

C4: New buildings are designed for a future climate, and opportunities for adaptation in existing buildings are taken during maintenance or retrofit. | |

|

C6: Coastal communities are preparing for and adapting to coastal erosion and sea level rise. | |

|

PS2: People can access the public services they need, and critical assets, systems and networks are resilient to the impacts of the changing climate. | |

|

Natural environment |

B2: Nature-based solutions are protected and enhanced to enable healthier, cooler, water resilient and nature-rich places. |

|

NC1: Landscape scale solutions are implemented for sustainable and collaborative land use including protecting and enhancing Scotland’s soils. | |

|

NC3: Development planning (including Local Development Plans and associated delivery programmes) takes current and future climate risks into account and is a key lever in enabling places to adapt. | |

|

NC4: Nature networks across every local authority area are improving ecological connectivity and climate resilience, alongside other transformative national actions to halt biodiversity loss by 2030. | |

|

NC6: Resilient natural carbon stores and sinks (such as peatland, forests and blue carbon) are supporting Scotland’s net zero pathway, alongside timber production, biodiversity gains, flood resilience and the priorities of local communities. | |

|

Transport |

PS4: The transport system (trunk roads, rail, |

|

PS2: People can access the public services they need, and critical assets, systems and networks are resilient to the impacts of the changing climate. | |

|

Water |

PS2: People can access the public services they need, and critical assets, systems and networks are resilient to the impacts of the changing climate. |

|

PS3: Partnerships for water resource planning and rainwater drainage networks are active in prioritised catchments to support climate resilient places and drought and flooding resilience. |

The sectors and sub-sectors included in our study are defined as follows:

Table 6 Sectors and sub-sectors explored within this analysis

|

Sector |

Sub-sector |

|---|---|

|

Agriculture |

|

|

Communities |

|

|

Natural environment |

|

|

Transport |

|

|

Water |

|

Note that, due to resource constraints, a range of other key sectors – for example, energy, telecommunications, and health – have not been explored in this report. Furthermore, even within the sectors we have examined, we have not conducted full sectoral analyses. For example, within transport, adapting ferries, aviation, and canals was not included in the analysis due to resource constraints. Consequently, the results should be interpreted accordingly.

Context setting

To estimate the uplift or scaling factors for adaptation investment needs to 2040, we considered how wider socio‑economic conditions, such as population change, economic growth and sectoral investment trends, might evolve over time. These factors can be important. For example, estimating future flood defence needs can require assumptions about future population distribution, while economic growth and inflation trajectories influence both the cost of adaptation measures and the scale of potential economic losses.

In practice, this broader socioeconomic context was only relevant to a limited part of our analysis. Most estimates relied on sector specific data and updated risk information – such as SEPA’s revised flood risk mapping or current housing stock – rather than the national socioeconomic scenarios developed for CCRA3. As a result, although we originally intended to use the central CCRA3 socioeconomic scenarios to inform investment scaling, these were largely not required in the final workflow.

If needed for future updates, this contextual information can be revisited, but for the purposes of this assessment it played only a minor supporting role.

Apportioning adaptation spend

Following the MDB taxonomy introduced in Section 2.2, this study applied different cost attribution approaches across the five sectors depending on the type of adaptation investment and available evidence. The specific methods used for each sector are detailed below and further elaborated in the sector-specific analyses (Section 4).

Climate-Proofing (Incremental Costs)

For infrastructure investments where adaptation is integrated into planned programmes but not the primary objective, we estimated incremental costs above baseline investment, for example:

- Transport (trunk roads and motorways): We applied relevant climate-proofing uplifts from the literature to Scottish Government 2026/27 budget lines for road maintenance and renewal. These uplifts reflect the additional investment required to design infrastructure for future climate conditions rather than historical baselines. For example, upgraded drainage capacity to handle more intense rainfall, enhanced slope stabilisation for increased landslide risk, or heat-resistant surfacing materials. The baseline represents the investment that would proceed regardless of climate change; the uplift captures the incremental adaptation cost.

Mixed Objectives (Apportioned Costs)

For investments delivering multiple benefits including adaptation, we apportioned costs based on expert judgment in consultation with Paul Watkiss Associates, who have extensive experience applying the MDB taxonomy internationally. For example:

- Woodland creation: Forestry investment delivers multiple benefits including timber production, carbon sequestration (mitigation), biodiversity, recreation, and climate adaptation (ecosystem resilience, water regulation, reducing downstream flood risk). We reviewed stated objectives in Scottish Government forestry programmes and applied expert judgment from Paul Watkiss Associates, aligned with on-going UK level adaptation investment need research, to determine what proportion of woodland creation costs should be attributed to adaptation.

- Peatland restoration: Peatland restoration similarly delivers carbon sequestration, biodiversity recovery, water quality improvements, and adaptation benefits (enhanced water storage and flow regulation reducing flood peaks, maintaining ecosystem function under climate stress). We assessed the relative emphasis on these objectives in Scotland’s peatland restoration programmes and apportioned costs, accordingly. These apportionments were cross-checked through expert review with Paul Watkiss Associates.

- Nature restoration: We applied similar logic to wider nature restoration funding, examining whether investments prioritise climate resilience objectives (e.g., creating ecological corridors to enable species migration under climate change, restoring coastal habitats for natural flood defence) or primarily target biodiversity and ecosystem health goals, and attributed costs proportionally.

Different analysts might reasonably apply different attribution percentages to the same mixed-objective investments, as there is no objectively correct answer to how investment should be apportioned across multiple objectives, including the distinction between climate adaptation and mitigation. The percentages applied in this study are therefore documented transparently in the sector-specific analyses (Section 4) and supplementary data.

Targeted adaptation (pure adaptation)

For dedicated adaptation investments where climate risk reduction is the primary or sole objective, we counted total programme costs: